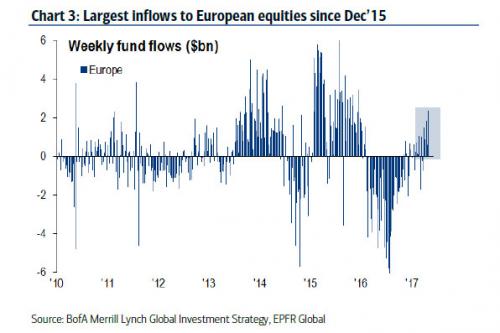

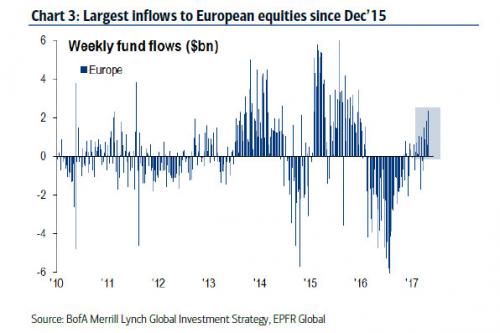

Forget the “great rotation” out of bonds into stocks: 6 months into the so-called reflation trade, which so many strategists predicted would unleash a new era of euphoric stock buying driven by bond sales, it just isn’t happening; in fact bonds have seen fund inflows on 17 of the last 18 weeks. Instead, two other “great rotations” have emerged: one out of “active management” into passive, or hedge funds to ETFs, while the other – more recent one – is out of various asset classes and into Europe. It was this last rotation that was on display in the past week, when Europe saw the biggest inflows – approximately $2.4 billion – since December 2015, and the 5th consecutive week of inflows in a row.

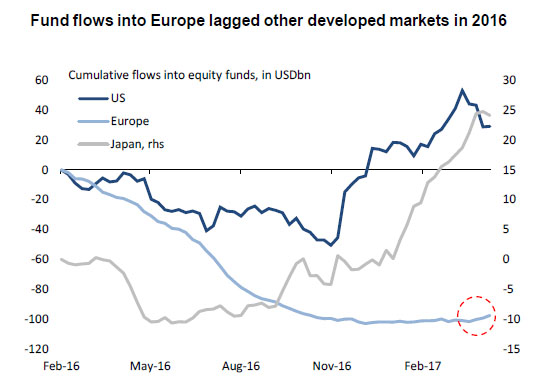

This is likely just the beginning: as DB observes overnight, “There is a wall of money just waiting to come into Europe”, as fund flows into Europe lagged other developed markets in 2016.

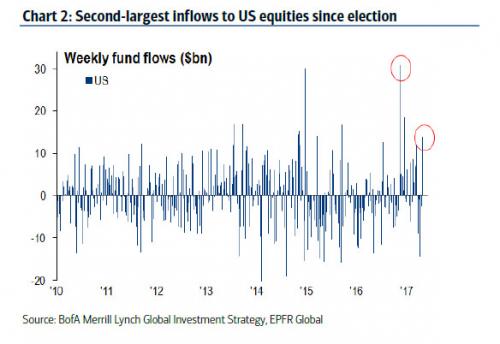

There were other notable observations in the latest weekly EPFR fund flow report. In addition to the surge in European inflows, a total of $21 billion was allocated to equities, the most since the US election on hopes Trump’s “tremendous” tax proposal could boost risk assets; instead it was a dud. The US alone saw $13.8bn in inflows, the largest inflows in 19 weeks.

Once again, there was bad news for active managers: of the $21 billion in equity inflows, $21.6 billion went to ETFs, which means that mutual funds suffered another $0.5 billion in outflows.If even on near record inflow weeks, the active community can’t catch a bid, it may be time to start thinking career alternatives. On a YTD basis, ETFs have seen $167 billion in inflows, offset by $45 billion in mutual fund outflows.

Some more observations on the latest fund flows, via BofA:

Leave A Comment