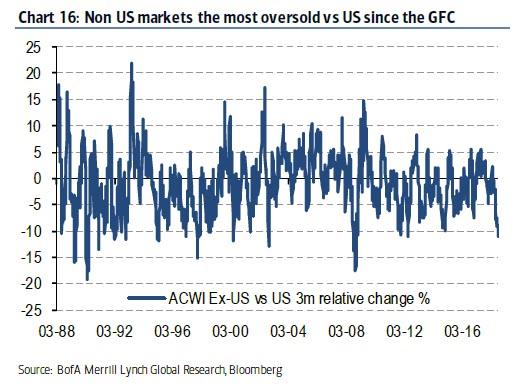

Last weekend we highlighted the most stunning divergence observed since the great financial crisis: non-US equity markets have underperformed the US the most over a 3-month period since the failure of Lehman, a divergence which Bank of America said”is reaching levels normally only exceeded in bear markets”.

This divergence, which has been observed across many other asset classes including commodities, Chinese stocks, European banks and others which have recently entered (and in many cases remained) in so-called “rolling bear markets”, is highlighted in the latest note by BofA’s Michael Hartnett who writes that global stocks ex-US tech are now down -6.2% YTD, while no less than 809 of 1150 EM stocks have entered a bear market.

But it’s not stocks that BofA is worried about, it’s bonds, and specifically, US investment grade BBB bonds which are annualizing a 3.2% loss (2nd worst since 1988), and which to Hartnett is the true “canary”.

And if the “canary” is indeed singing – if remains ignored by US stock markets – there is one reason, and it’s very simple: according to Hartnett one should “Buy when the central banks buy, sell when…”

Indeed, so far the tailwind from global QE is still here and has resulted in record global EPS, 4% US GDP, $1.5tn US tax cuts, $1tn stock buybacks… yet poor 2018 returns.

The reason is a familiar one: the liquidity supernova is going into reverse, i.e., the “end of excess liquidity:”

End of excess returns: CB’s bought $1.6tn assets in 2016, $2.3tn 2017, $0.3tn 2018, will sell $0.2tn in 2019; liquidity growth turns negative in Jan’19 for 1st time since GFC.

Which brings us back to the topic of rolling bear markets, or as Hartnett dubs it: “Bitcoin to Popcoin”, or a world in which the bursting of the Bitcoin bubble may have been the first domino:

Leave A Comment