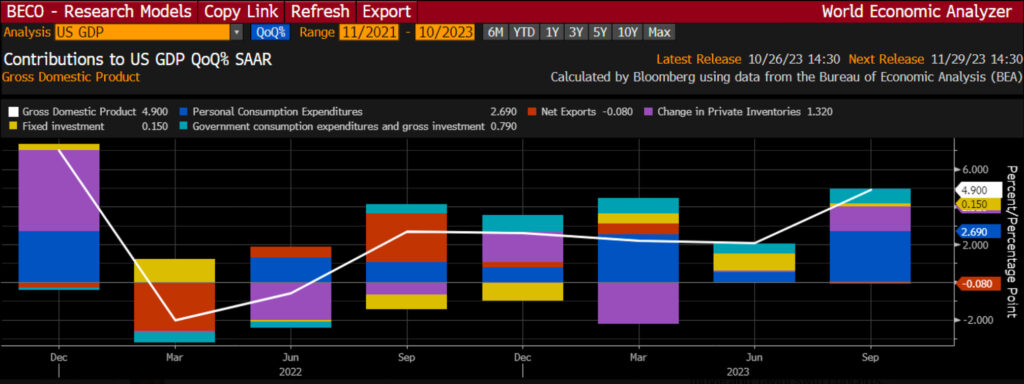

Q3 GDP came in at a boomy 4.9%. The chart at the right breaks down the contributions by component. The primary drivers were inventories and personal consumption at 1.3% and 2.69%. The inventory rebuild is a volatile component, but the consumption figure is impressive and reflects the most important component of GDP.The US consumer has been remarkably resilient in the face of many different headwinds. But the market didn’t seem to like the data so much. Or rather, the market is looking beyond the data.The big GDP figure didn’t exactly surprise analysts. After all, the Atlanta Fed’s GDP Now forecast has been over 5% since August so the market appears to be selling the news and looking forward. Bloomberg Economics has very early Q4 GDP estimates at just 1.1% so some giveback is likely coming. Still, the recession that many analysts expected did not come to fruition. Or, at a minimum, the slowdown in growth hasn’t been as extreme as expected.Interestingly, the S&P 500 is down 10% since that first GDP Now print came in over 5%. Of course, the economy is not the stock market, but the market appears to be sniffing out something that isn’t being reflected in current data like GDP. Our guess is that the market is sniffing out how impactful the recent surge in interest rates is going to be. As I’ve noted for well over a year now, the real risk with the Fed and inflation is that they end up tightening further for longer. The longer they remain tight the more credit markets grind to a halt. And more and more contracts have to roll over at newer and more punitive rates. And although the Fed has been raising rates for well over a year now, credit markets have only been tight for about 6 months now. The first 3-4% of rate hikes were just the Fed playing catch up. But when the Fed moved over 4% credit markets started to tighten meaningfully and have only tightened further since.With mortgage rates surging over 8%, it’s reasonable to expect fixed private investment to slow again after a brief resurgence earlier this year. And consumption relies largely on employment which has been trending slower for some time now. The recent jump in continuing jobless claims is not alarming, but it is consistent with a slowing labor market. If credit markets continue to tighten labor will slow further and the market is currently trying to sniff out how meaningful that risk is.More By This Author:Inflation Hedges, Bonds And The “This Is Fine” EconomyChart Of The Week – The Broken Housing Market (That Isn’t Broken) Weekend Thoughts – SBF, Interest Rates & Jobs

Q3 GDP came in at a boomy 4.9%. The chart at the right breaks down the contributions by component. The primary drivers were inventories and personal consumption at 1.3% and 2.69%. The inventory rebuild is a volatile component, but the consumption figure is impressive and reflects the most important component of GDP.The US consumer has been remarkably resilient in the face of many different headwinds. But the market didn’t seem to like the data so much. Or rather, the market is looking beyond the data.The big GDP figure didn’t exactly surprise analysts. After all, the Atlanta Fed’s GDP Now forecast has been over 5% since August so the market appears to be selling the news and looking forward. Bloomberg Economics has very early Q4 GDP estimates at just 1.1% so some giveback is likely coming. Still, the recession that many analysts expected did not come to fruition. Or, at a minimum, the slowdown in growth hasn’t been as extreme as expected.Interestingly, the S&P 500 is down 10% since that first GDP Now print came in over 5%. Of course, the economy is not the stock market, but the market appears to be sniffing out something that isn’t being reflected in current data like GDP. Our guess is that the market is sniffing out how impactful the recent surge in interest rates is going to be. As I’ve noted for well over a year now, the real risk with the Fed and inflation is that they end up tightening further for longer. The longer they remain tight the more credit markets grind to a halt. And more and more contracts have to roll over at newer and more punitive rates. And although the Fed has been raising rates for well over a year now, credit markets have only been tight for about 6 months now. The first 3-4% of rate hikes were just the Fed playing catch up. But when the Fed moved over 4% credit markets started to tighten meaningfully and have only tightened further since.With mortgage rates surging over 8%, it’s reasonable to expect fixed private investment to slow again after a brief resurgence earlier this year. And consumption relies largely on employment which has been trending slower for some time now. The recent jump in continuing jobless claims is not alarming, but it is consistent with a slowing labor market. If credit markets continue to tighten labor will slow further and the market is currently trying to sniff out how meaningful that risk is.More By This Author:Inflation Hedges, Bonds And The “This Is Fine” EconomyChart Of The Week – The Broken Housing Market (That Isn’t Broken) Weekend Thoughts – SBF, Interest Rates & Jobs

Leave A Comment