Critics of today’s fiat currency/fractional reserve banking world have (for what seems like forever) made the common sense point that when debt rises faster than cash flow, bad things are bound to happen. In every cycle since 1980 this has been dismissed by the vast majority who benefit from inflating bubbles — until the bubble bursts.

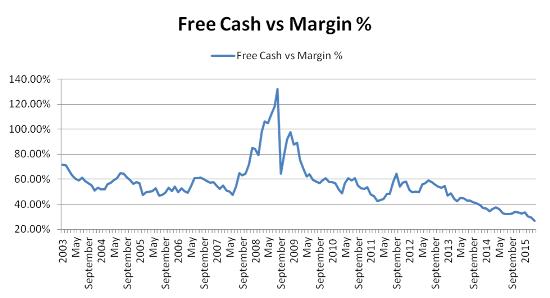

And here we go again. The following chart from Stock Traders Daily shows the relationship between margin debt (money borrowed by investors against existing stock positions in order to buy more stock) and cash on hand in brokerage accounts. The idea is that when investors hold lots of cash they’re pessimistic, and when they borrow a lot they’re optimisitc. Extremes of either tend to signal changes in market direction. At the end of 2015 investors were even more excited than at the peak of the housing bubble, indicating that there’s not much retail money left to be tossed at US stocks.

China, being a little more bubbly than the US, is a good indicator of where US margin debt might be headed:

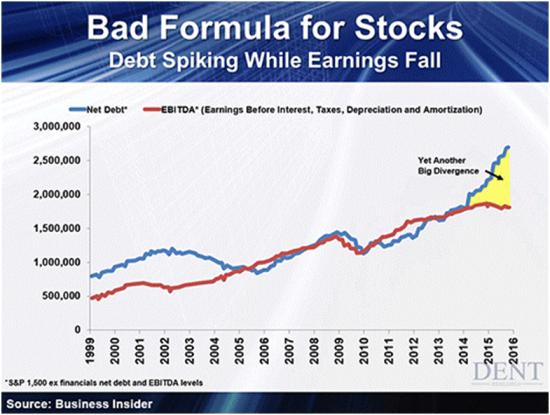

Another red flag is being waved by corporate debt, much of which is being taken on to fund share repurchase programs. These tend to benefit shareholders in the moment but at the cost of higher leverage and less flexibility in the future. Where in the past net debt has tended to track EBITDA (a broad measure of earnings). starting in 2014 the former has soared beyond the latter. Just as a spike in margin debt implies a lack of retail stock buying in the future, soaring corporate debt implies limited borrowing power and a scale-back of share repurchases going forward.

Based on both history and common sense, we should expect not just a slowdown, but a cratering of equity demand from both individuals and corporations in the year ahead. What happens then? Either the market crashes and prices go back to levels that attract wiser capital, or a new source of dumb money emerges.

Leave A Comment