Financial Sense Newshour just spoke with Craig “Bullseye” Johnson from Piper Jaffray to get his outlook on the market.

Johnson believes the corrective phase that started in February is not over and provided some downside targets for the S&P 500. He’s also positive on the energy complex and noted a possible shift away from FAANG stocks.

Here’s what he told Financial Sense Newshour listeners on Saturday…

Current Red Flags

We’ve now entered a correction phase, Johnson said, and expectations are in the process of being reset.

“A corrective move back down toward 2,500 to 2,350 (on the S&P 500) is becoming more likely,” he stated.

Source: StockCharts.com.

Past performance is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly

A few other factors have been building concern in market participants as well. For one, the 10-year yield recently crossed 3 percent, where just a short while ago, we were hearing concerns about a possible yield curve inversion.

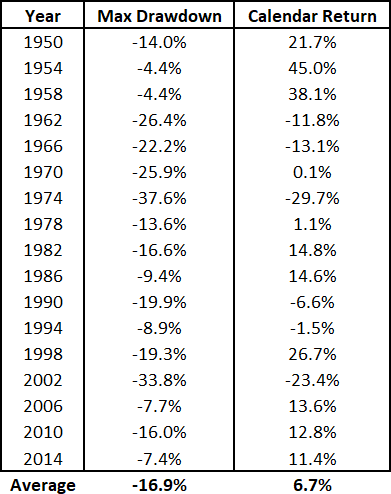

We’re also in the second year of a first-term president with midterm elections around the corner, which, historically speaking, tends to be a more volatile time for the market.

S&P 500 Mid-Term Election Drawdowns and Annual Returns

Source: Bloomberg, Financial Sense® Wealth Management. Past performance is no guarantee of future results. Please note: The modern design of the S&P 500 stock index was first launched in 1957. Performance back to 1950 incorporates performance of the predecessor index, the S&P 90.

Another important factor Johnson noted is that even with terrific first quarter earnings, the reaction by investors was sub-par and many leading companies failed to break out to new highs.

The problem for the market now is that it seems to be at a loss for determining what will drive the market higher in 2018 if the strong earnings growth hasn’t been able to do the trick. One can argue, incidentally, that the projections for strong earnings growth this year pulled 2018 returns forward into 2017 and helped catalyze the January rally as a fear of missing out on further gains led to some speculative buying interest. The fear now, then, is that the earnings fix is in and that rising input and labor costs are going to break things. (terrific first quarter earnings)

Leave A Comment