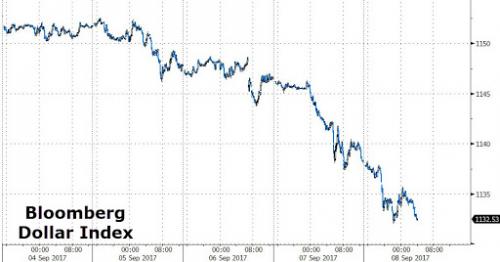

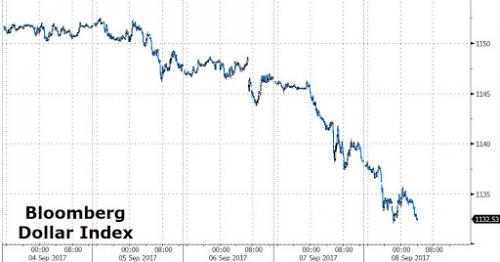

European stocks dropped, Asian and EM market rose, and S&P were lower by 0.3% as investors assessed the latest overnight carnage in the USD which plunged to the lowest level since the start of 2015, sending the USDJPY tumbling to 107, the euro extending gains to just shy of $1.21 and a slowdown in China’s export growth which however did not prevent the Yuan from posting its best weekly gain on record.

It was all about the seemingly huge currency moves overnight as the dollar plunged for the 7th day in a row, the biggest 7 day drop in 4 months, amid doubts about further Federal Reserve tightening, North Korea tensions and as Hurricane Irma threatens South Florida.The Yen rose to the strongest level against the dollar since Nov. amid nervousness about possible provocation from North Korea ahead of its foundation day on Saturday; yen surged past 108 per dollar as options barriers gave way, triggering a series of stop-losses. The Yuan rallied toward 6.45/USD in both onshore and offshore markets as traders speculate PBOC will tolerate a stronger currency after it rose past the psychological 6.50 mark Thursday. The Australian dollar surged to the highest in more than two years on the back of dollar weakness while the cherry on top was the 10Y TSY yield touching a YTD low of 2.014% before rebounding to ~2.035%.

Meanwhile, natural disasters were aplenty, including the most powerful earthquake this century to shake Mexico, while Hurricane Irma is projected to hit Florida Sunday, and North Korea is widely expected to launch an ICBM on its September 9 holiday.

As latest overnight carnage in the USD, the big overnight story was the dramatic plunge in the dollar in Asian trading….

… which also pushed the EURUSD to the highest level since January 2015, a move that was not helped by this morning’s Reuters “trial balloon” according to which the ECB was considering 4 QE reducing scenarios.

“At its current level, the Euro is not a threat for the Eurozone,” Philippe Ithurbide, global head of research at Amundi Asset Management, said in a report. “If the euro stabilizes, or continues a gradual appreciation path as in our base scenario, the ECB could announce — maybe in October — a reduction, starting in January 2018, of the quantitative easing program. Should the euro continue to appreciate rapidly, the ECB could become more dovish and postpone its tapering.”

This morning, the USD has attempted to stabilize after said heavy selling in Asian session, which has seen the DXY hit a fresh YTD low. Meanwhile, the USD/CNH has bounced from levels last seen in Dec. 2015 after reports of Chinese concerns on yuan strength.

According to Reuters, China policy makers are increasingly worried a sharp CNY rally could hurt exports and the economy, however China is unlikely to intervene forcefully to cap the CNY due to worries of criticism from the US.

Overnight, NY Fed president Bill Dudley became the latest U.S. central banker to lay out his views ahead of a policy-setting meeting later this month as expectations for an interest-rate increase have been scaled back. According to Bloomberg, Dudley reiterated the need to continue raising rates while conceding that the Fed may have to rethink its inflation model.

USD/JPY holds close to overnight levels after tripping downside stops through 108.00. As this morning’s Reuters “trial balloon, Bund futures sell off after latest ECB sources give more details on potential tapering, curve steepens. Treasurys partially retrace overnight spike higher, precipitated by the USD weakness.

In equities, European equity markets open lower and slowly grind back to unchanged led by bank sector, Santander +2.5% after being upgraded at Morgan Stanley. Mining sector underperforms after base metals sell offaggressively in response to China trade data. Stocks in Europe struggled for traction as the euro extended its march above $1.20, while S&P 500 index futures dropped. The most powerful earthquake this century shook Mexico, adding to investor anxiety.

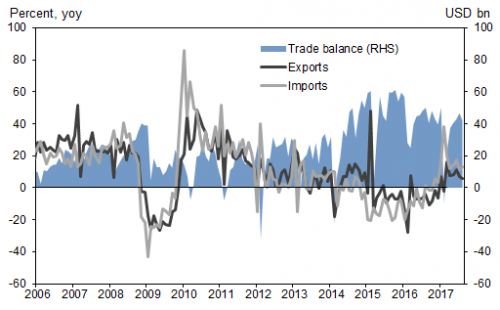

Asia equity markets traded mixed following similar indecisiveness in US and as the region digested a slew of economic releases including Japanese GDP and Chinese Trade data. ASX 200 and Nikkei 225 were lower as financials mirrored the underperformance in their US peers, with Japan also dampened by a weaker than expected Final Q2 GDP which showed the largest downward revision since the current accounting method began in 2010. Shanghai Comp. and Hang Seng were positive despite another OMO skip by the PBoC which resulted to a larger net weekly liquidity drain W/W, as strength in property and energy names kept sentiment upbeat while traders mulled over the release of mixed Chinese Data. China released its latest trade balance data which showed that Exports missed, but Imports surpassed expectations to suggest strong domestic demand. Exports growth for China moderated to 5.5% yoy in August from 7.2% yoy in July, below expectations, while imports growth was up to 13.3% yoy from 11.0% yoy in July, above consensus. In sequential terms, exports contracted by 0.4% mom sa, albeit less than that in July ( -2.0% mom sa). Imports increased by 2.9% mom sa, rebounding from -1.9% mom sa in July. The trade surplus moderated to US$42.0bn from US$46.7bn in July

Meanwhile, the threat from North Korea lingers. U.S. President Donald Trump said it’s not “inevitable” that the U.S. will wind up in a war with North Korea over its continued development of nuclear weapons, though military action remains an option. Pyongyang may test a missile this weekend to coincide with its “founding day” on Sept. 9.

Ten-year Treasury yields fell toward 2 percent and gold headed for a third week of advance ahead of a potential North Korean missile launch. Copper led most industrial metals lower and crude oil dropped. The yield on 10-year Treasuries declined less than one basis point to 2.04 percent, the lowest in 10 months. Britain’s 10-year yield advanced one basis point to 0.982 percent.

Leave A Comment