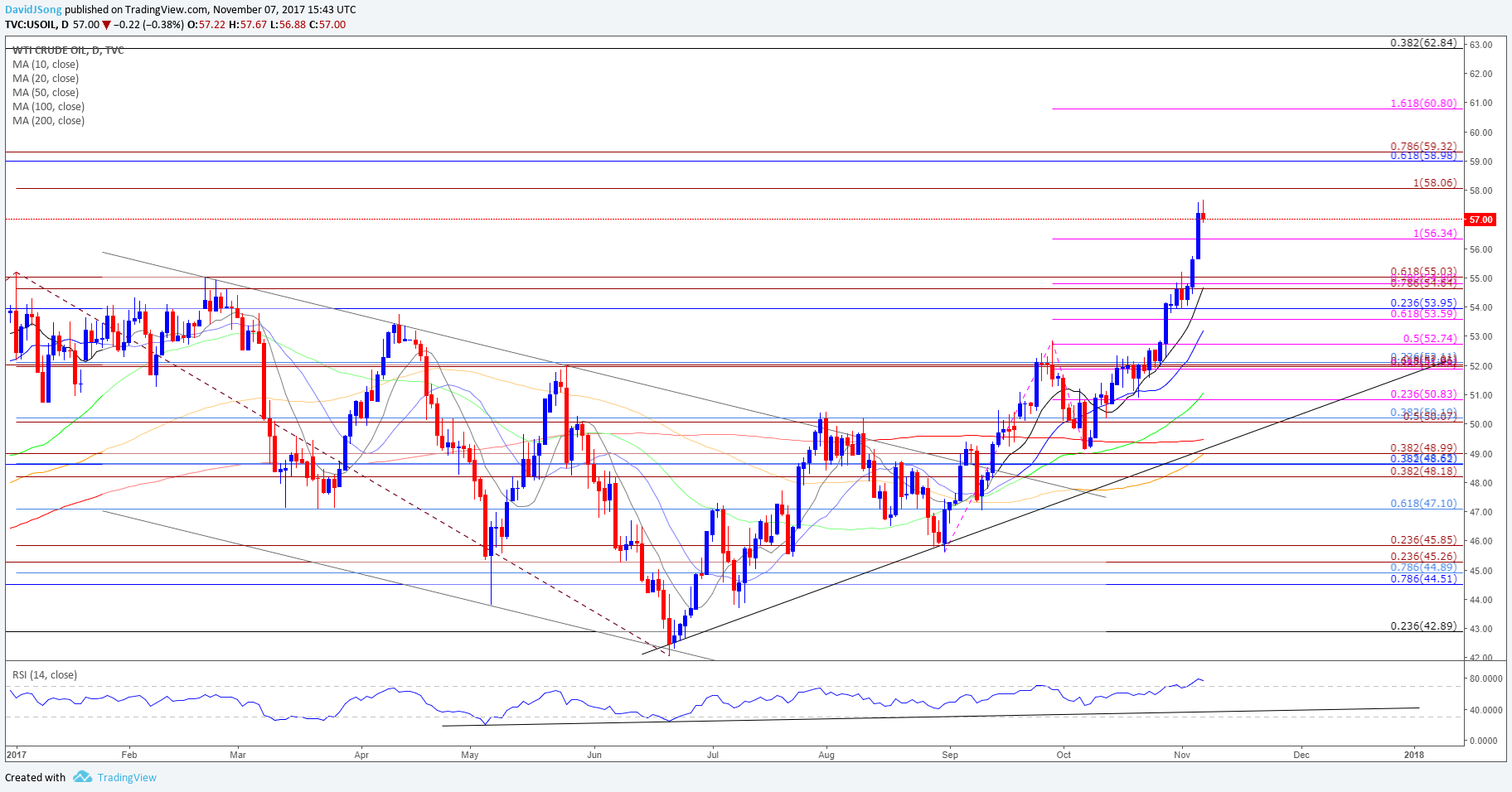

Crude rallied to $57.67 after unexpectedly breaking the January-high ($55.21) at the end of the previous week, and oil prices may stay bid ahead of the Organization of the Petroleum Exporting Countries’ (OPEC) next meeting on November 30 as Relative Strength Index (RSI) pushes into overbought territory for the first time in 2017.

With OPEC and its allies largely committed to rebalancing the energy market, it seems as though the group will extend the output cuts beyond March 2018, but the pickup in crude oil prices appears to be having an adverse effect as the Monthly Oil Market Report (MOMR) for October warns higher prices ‘would encourage US oil producers to expand their drilling activities.’

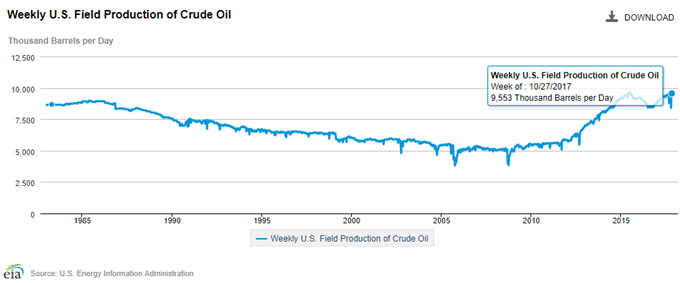

Keeping in mind, U.S. field production sits near the 2017-high (9,561) even as crude inventories are projected to narrow another 2708K in the week ending November 3. In turn, market participants may pay increased attention to the ongoing expansion in U.S. output as ‘the main factors for higher growth expectations for the remaining month of 2017 compared to last year are the current improving price environment, which is more suitable for shale producers.’

USOIL Daily Chart

Leave A Comment