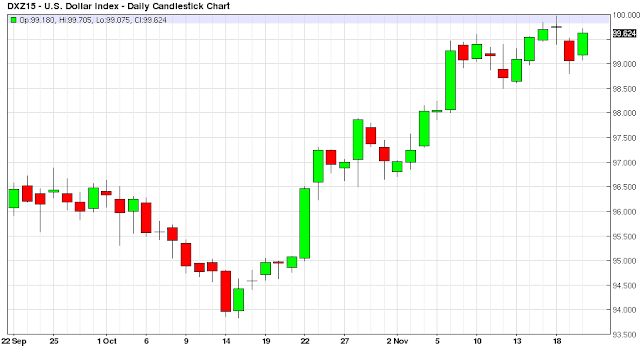

One of the most common trades in financial markets these days is going long the US Dollar and shorting Commodities, especially the precious and industrial metals. This has been a bad year for commodities, and this trade has picked up steam with large fund flows the last 6 weeks.

Schizophrenic Fed & Employment Reports

This all turned around after the poor employment report of October 2, followed by some trade unwinding thinking the Federal Reserve may be on hold for the remainder of the year after the dismal October Employment Report. This resulted in about eight days of currency unwinds and around October 14, investors started putting the Long Dollar Trade back on as they realized the Fed still wanted to raise rates, and since China seemed to stabilize from a crashing standpoint, Fed Speak became hawkish to telegraph to financial markets that the December meeting was a potential live meeting for a rate rise. This trade really picked up speed when the November 6 Employment Report came in much stronger than anticipated with a robust 271,000 new jobs created for the previous month.

Trading Algos & Paper Markets

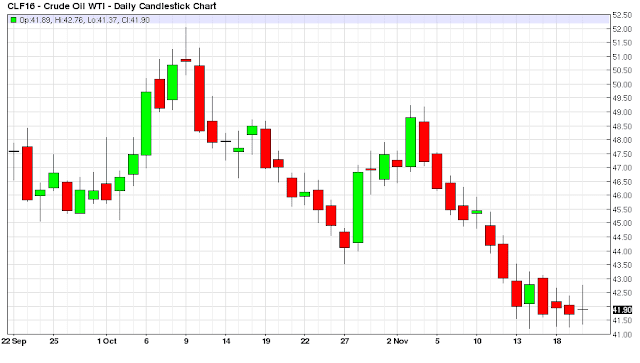

Oil has also been hit along with the metals but it has inventory issues to contend with and is in the midst of a price war for market share. But there is no such price war in the metals industry, and although China`s weakness has no doubt tempered demand, the precious and industrial metals are basically being hammered down in the paper markets by fund flows in this Long Dollar Trade. This trade has become such a reflexive trade, that if the US Dollar is strong, the trading algos just start attacking Gold, Silver, Copper, Aluminum, Platinum and Palladium. These metals by and large trade as a group with slight differences in the charts based upon any unique demand characteristics of the given metal.

Soft Demand

Demand hasn`t really fluctuated much for any of these metals the last six weeks, China and the global economy are just sort of trudging along with China`s rebalancing and the global economy growing somewhere in the area of 3.5%. But what has changed the last 6 weeks is the large fund flows into the US Dollar all trying to front run the Federal Reserve, and shorting the Euro, (which makes up the largest component in the US Dollar Index), with traders also front running Mario Draghi who has been telegraphing more future stimulus for the European Union.

Leave A Comment