The preliminary February US Durable Goods report wasn’t exactly a strong report despite beating expectations, and helped keep the US Dollar’s intraday pullback in place. While the headline figure was ‘above expectations,’ the prior month’s data were revised lower, creating an illusionary base effect.

Accounting for these statistical quirks, it’s clear that US consumers are only muddling along. After all, durable goods – items with lifespans typically three-years or longer, which usually translates into more expensive appliances – are a bellwether for growth. Consumers typically only make large outlays when they feel secure about their finances; and the fact that durable goods orders remain weak suggest that Q1’16 growth should be capped around +2% annualized.

Here are the data that’s keeping the US Dollar pinned lower this morning:

– USD Durable Goods Orders (FEB P): -2.8% versus -3.0% expected, from +4.2% (revised lower from +4.7%) (m/m).

– USD Durable ex Transportation (FEB P): -1.0% versus -0.3% expected, from +1.2% (revised lower from +1.7%) (m/m).

– USD Initial Jobless Claims (MAR 19): 265K versus 269K expected, from 259K (revised lower from 265K).

– USD Continuing Jobless Claims (MAR 12): 2179K versus 2235K expected, from 2218K (revised lower from 2235K).

See the DailyFX economic calendar for Thursday, March 24, 2016

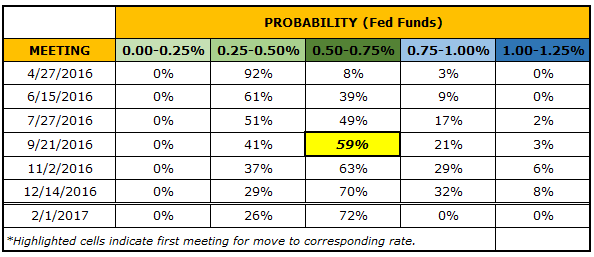

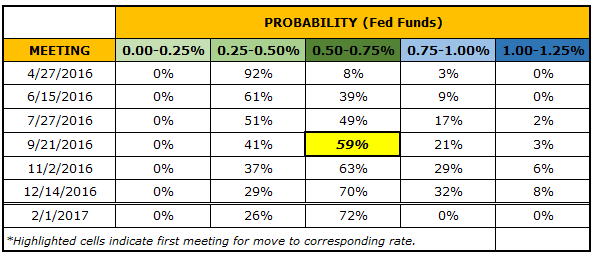

Table 1: Fed Funds Futures Contract Implied Probabilities: March 24, 2016

Following the data, market participants aren’t taking the figures as a collective sign that the Federal Reserve will be raising rates in the first half of the year; September is currently being priced-in as the most likely period for the next rate hike. There is currently a 39% chance of a rate hike in the first half of this year, and only an 8% chance for one in April, per the Fed funds futures contract.

It’s worth noting that, historically, the Fed hasn’t raised rates unless the implied pricing for the front month meeting (in this case, April) has been above 60%. Needless to say, if Fed officials continue to talk up the possibility of a rate hike in the first half of this year, there’s a bit of room for rate expectations to tighten up which chould prove to be supportive of the US Dollar henceforth. We’ll be keeping an eye on retail trader positioning for a turn in the US Dollar – follow SSI updates live here.

Leave A Comment