Video length: 00:09:48

The US Dollar (via DXY Index) is trading right back to its weekly open, as a lack of clear drivers on the calendar leaves the greenback waiting for catalysts to cross the news wires. The greenback isn’t alone in this endeavor, as neither the British Pound nor the Canadian Dollar nor Euro have data releases due out that could be considered “materially important.”

While there may not be any data worth paying attention to the remainder of the week, the specter of tax reform legislation has been, and will be, the key source of influence for the US Dollar in the days ahead – particularly before the Thanksgiving holiday in two weeks, when an unofficial, soft deadline for tax reform has been set by Republican leadership in Washington, D.C.

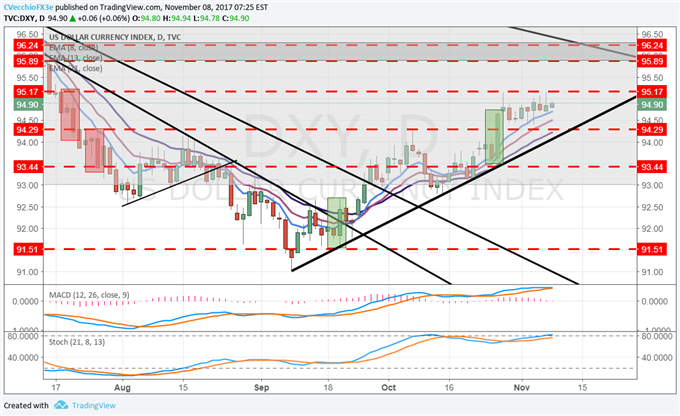

For now, this leaves the DXY Index playing ping pong between two key levels, 94.29 (the neckline of the inverse head & shoulders pattern, as well as the July 26 bearish outside engulfing bar high) and 95.17 (the July 20 bearish outside engulfing bar high).

Since trading into this range on October 26, the DXY Index has yet to close outside of it. Generally, while the DXY Index’s technical posture remains bullish (price above the daily 8-, 13-, and 21-EMA envelope, and MACD and Stochastics in bullish territory), this may not be the time to establish fresh longs as we wait for resolution of the near-term range.

Chart 1: DXY Index Daily Timeframe (July to November 2017)

Elsewhere, focus should stay on the Asia-Pacific region as it has thus far this week thanks to the other of the two major central bank decisions concluding before markets close in the US for the day. The Reserve Bank of New Zealand’s November policy meeting (today in New York, tomorrow in Wellington)

Once again, the main way the RBNZ has the potential to hit the Kiwi is via commentary on the exchange rate. In the meetings since June, the RBNZ has noted to some extent that “A lower New Zealand dollar would help rebalance the growth outlook towards the tradables sector.”

Leave A Comment