A ‘desperate secondary test’ just above the January 20 lows preceding our expected ‘reflex rebound’, and ensuing decline from February’s start, is really the core message to convey about Monday’s market turnaround try. It’s dicey; has little prospects for success, and is discussed (and projected from technical perspectives) to be part of the pattern ‘process’ outlined for weeks.

The reason I begin with this is unusual: despite the obvious nature of trying to hold above the preceding low (and thus seeking to avert a penetration into what I call ‘no-man’s land’ that lies below), the pundits are either rationalizing a turn as bargain-hunting (little of that); or short-covering (lots of that); or based on oil being strong (sort of, but lots more challenges, dividend cuts and defaults loom both here and abroad); or somehow a rebound in Financials (that was solely a function of late-day post-European market close statements by Deutsche Bank (DB), the institution at the heart of Europe’s banking fears, saying they have sufficient liquidity to meet a Coupon payment in April).

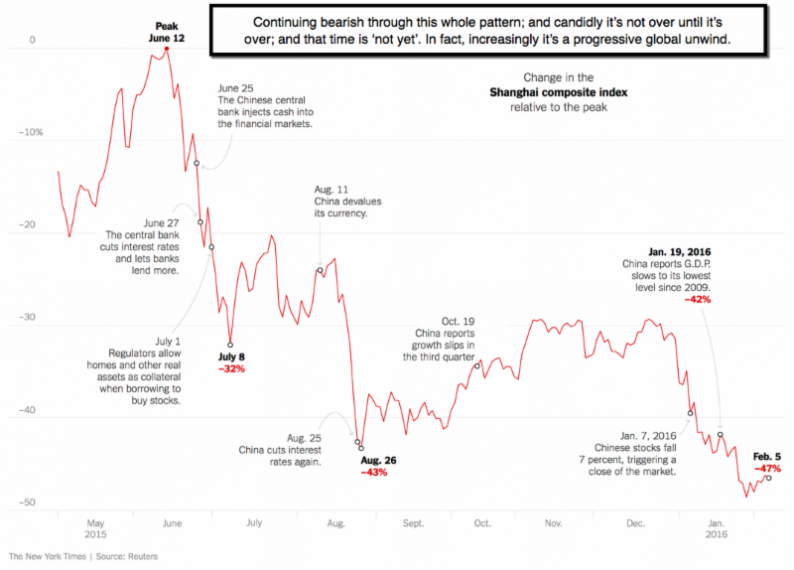

This matters, because ‘some’ would act ‘as if’ the market simply turned around (it tried but was goosed-along by DB), because investors saw bargains. That’s nonsense, though there’s no argument the lower things go the lower the risks. I should also say that while others are suggesting we ‘may’ enter a recession in the future, I contend we are in one roughly since indicated in July of 2015. That makes me ‘more’ optimistic about getting this ‘Bear Market’ over with earlier if you think about it, than many suggest. Here I’m referring to ‘lead times’ during which a market sees distribution (all last year) and then the lag for a recognition formally of a recession (closer to the end historically). Because at that point the stock market starts anticipating the recovery that follows.

Leave A Comment