Banks are wrapped-up in an enigma… unrelated to the lack of transparency about Chair Yellen’s testimony coming right up; but perhaps fearful of a concern which we have already expressed: negative interest rates.

That’s why we pleaded, when we heard (and shared) rumors over a week ago that US banks would be asked to initiate stress tests to see ‘how they’d do’ in a ‘negative yield environment’. We saw that as a ‘trial balloon’, and in today’s last hour they trotted-that out again. The timing was perhaps intended to coincide with a few minutes left in Tuesday’s NYSE action to see how the statement was received; perhaps preparing the markets for a dovish testimony from Yellen. If they expected a favorable response they didn’t get it; the S&P quickly reversed, albeit not dramatically. Central bankers want citizens (they call us consumers of course) to spend spend spend, and not save. They think that will revive a fairly lame economy; while they fail to realize ‘the people’ want fiscal responsibility.

Perhaps that’s why the candidates leading voters in both parties seem vaguely distant to the establishment; as basically the people (liberal or conservative or just normal middle class Americans) are essentially saying they’ve had enough.

And in this case I suspect it’s not a nod to denying opportunity, but the opposite as well as demanding a tight purse and diminished debt by Government. Yes it may seem that doesn’t go along with some broader programs; but the point is it is just a reflection of moods out there. We focus on markets but aren’t oblivious to societal agitation, which while not like Hong Kong (and yes I mentioned that last night hours before hearing about actual clashes in the streets; coincidence) we have had a period of time of leadership polarizing not uniting people; of that I think both parties are indirectly saying, enough. Let’s move forward and grow.

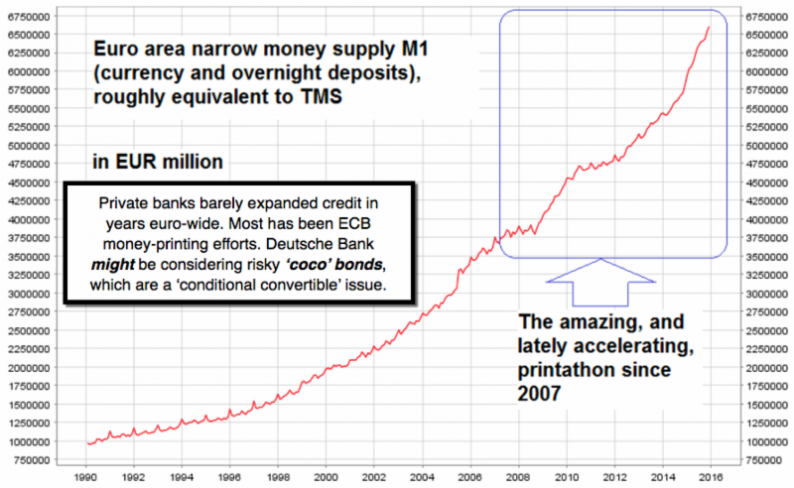

But doing so will not be accomplished by moving to negative interest rates, and what I feared (because Japan, China and ECB are doing it); more of the same bad medicine to cure a problem that they perhaps naively continue feeding. So the upcoming Fed testimony takes on more than the usual prospects of being a defense of Fed policy (which they should at this point); but risks a ‘caving-in’ or sort of mea cuppa about the Fed’s recent moves. They were late, backfired just as I thought they would; but we expected the Fed to do it. They really needed a move away from the money-printing philosophy; today’s ‘hint’ suggests they do not yet ‘get it’, and I hope that during the testimony we learn that’s not the case.

If it’s very dovish the market will try to grab onto it, but then sell into it. If it isn’t the case, the market may try to cull-out key words like ‘data-dependency’ to try to get some market upside going. So it’s tough (impossible) to read her mind at this point. It is possible to proclaim that any solid rally will get sold into.

Yes the outcome may take this market to lower levels; even if by a circuitous or up-down-reversal route. If they ‘go Japanese’; the exact concern we expressed last week (yes we’ve been correctly bearish on distribution and trends, and see a stupid move by the Fed as just further enhance our downside gains. But, as a citizen wanting to see America distinguish itself above grovelling monetarists, I wanted to see something supporting the idea that Stan Fischer and Yellen were going to ‘rise above’ the frey of pulling-out all the stops to push people into both spending and risk-taking modes. This is the ‘let’s pour more gasoline on a fire’approach; and it’s uninformed, borders on panic desperation, and it won’t work. And yes it remains unconscionable to push risk-averse citizens into taking risk; an absolutely abysmal situation prevailing for fixed-income retirees for years.

We already had Japan’s reaction; and it was briefly up then tanked. We already heard Deutsche Bank a week ago pleading with the ECB ‘not’ to keep cutting; as the message to ECB from DB was: you’re killing us. So what do we get? Out of DB not much response (up early then down in Europe overall) to their sort of sad necessary statement of ‘rock solid stability’ (such statements usually bring a degree of concern from depositors who otherwise don’t even think about it).

I of course do believe DB will be around; they are the State bank basically. We have talked about their noble if risky loan portfolio for quite a long time. General perceptions hold that US banks have been reserve provisions than European in an overall sense; and that’s why the others like Barclays and Credit Suisse are under pressure, as investors examine all the major banks. I haven’t heard lots of discussion about the different nature of the lending practices that we noted. It also ‘may’ be that the US Fed wants to show our strength relative to Europe via the ‘stress tests’ on negative rates. If that’s all; fine; but there are Fed officials in candid conversations who chatter about actually doing it. That is foolish, as I’d commented earlier in the day about the retired Minneapolis Fed President, who actually advocated negative rates this morning, hours before the ‘trial balloon’.

Bottom-line: I quoted a former Fed President calling for negative rate policies; and called that folly (in a sense hoping the leaders were beyond that). No such luck I’m afraid; as they are foolish enough to take us more Japanese.

I know that a ‘stress test’ doesn’t mean they’ll go to negative rates; but it’s really sad that they are even doing that. After all, the perception is that US banks are in better shape than European banks; so if this is an attempt to move the topic away from the loan-loss exposure to the Energy industry; I suspect it will fail to deviate attention to ‘rates’, but rather increase the concern of something wrong.

In-sum: market technical factors are unchanged; the proximity to breakdown remains of course; with oil stocks hinting at some temporary basing, since the market largely ignored the Anadarko Petroleum dividend cut; suggesting such cuts largely are priced-in. Hope so; but need to see more. And you have new and large across-the-board inventory builds reported late Tuesday.

On negative rates, one member put it fairly succinctly (although I believe goes to the overall debt structure the money-printing has created), but says it clearly: ‘It’s all artificial central bank steroid injections and it will either kill the patient if continued or once discontinued the patient implodes back to its natural size. It won’t be pretty either way.’

Leave A Comment