The surge in U.S. long-term interest rates has long been desired as a sign of strong economic growth, yet it does not come about without consequences. Central banks are constrained by the limits on how much they could reduce short-term interest rates to promote growth. They were forced to develop policies that would affect long-term rates. While the financial markets look to changes in short-term rates as a sign of changing financial conditions, the more important action takes place in the long end of the yield curve. Long-term interest rates determine business spending decisions on capital investments and consumer decisions on home purchases. To combat the effects of the 2008 financial crisis, the Fed zeroed on the need to lower long-term interest rates to encourage asset purchases.

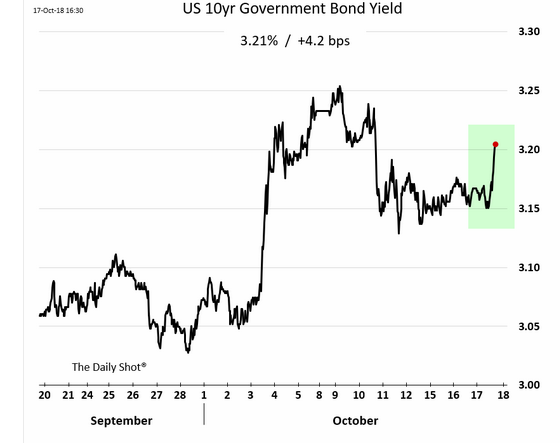

Now, the Fed is reversing course. It is both tightening short-term borrowing costs and, at the same time, shrinking its balance sheet. Although these forms of tightening have been underway over the last 2 years, the bond market has been slow to react with higher long-term rates, until this month (Figure 1). The Fed wanted to encourage investors to buy risky assets when it introduced quantitative easing. Now it seems the Fed wants to rein in risk-taking and welcomes the significant increase in the 10-yr bond yield.

Figure 1 US Long Rates

One school of thought argues that the rise in long-term rates is a positive development as it signals that the economy is strong enough to withstand higher borrowing costs. Normalization can take place without harming the economy. Rising nominal and real rates of interest reflect investors’ confidence in future growth. However, we are now witnessing another side of this story.

A Weakening Housing Industry. Housing starts fell 5.3 percent to a seasonally adjusted annual rate of 1.201 million units in September. The Homebuilders Index, already sagging during the summer, took another leg down in October and now resides some 40% lower for the year as a whole (Figure 2). As mortgage rates top 5%, housing affordability has become the major challenge to sustaining residential investment. In terms of impact, rates have increased by 90bps this year, denying thousands of first-time buyers an opportunity to purchase homes.

Leave A Comment