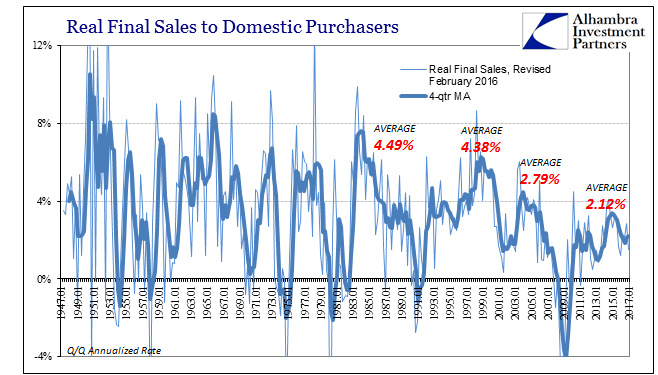

The internals of the GDP report were as ugly as the headline. The major source of weakness was what was supposed to be the sole source of strength – consumers. Real Final Sales to Domestic Purchasers, a measure of all goods and services Americans bought regardless of where they originated, increased by just 1.51% (quarter-over-quarter annual rate) in Q1. That was the lowest result since Q1 2016 and continuing to suggest no recovery at all in US “demand” from the now-unquestioned weakness of the “rising dollar” period.

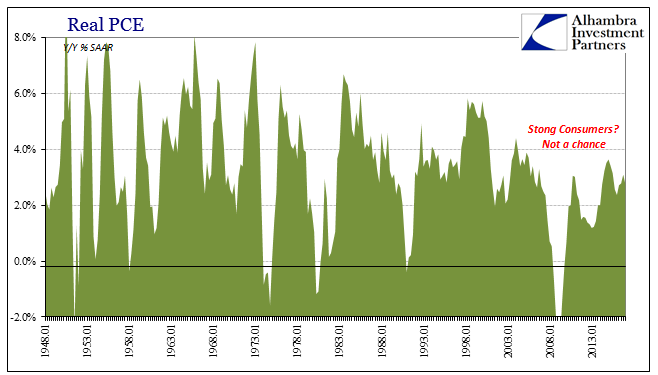

Real Personal Consumption Expenditures were barely more this quarter than last (+$10 billion, or +0.08%), as the PCE Deflator’s oil-inspired rebound subtracted a significant amount. Translating the statistics into the real world economy, the rise in gasoline prices, largely, crowded out spending in other places, leaving consumers without the ability to contribute anything to an expanding economy.

Lingering problems in consumer spending really should not be surprising given labor statistics over the past year and a half. Even the Establishment Survey has registered some level of significant slowing over that time, and despite the unemployment rate fully less than what was supposed to be “full employment” there isn’t even a small suggestion of wage inflation.

That is, of course, a problem all its own but especially one at this juncture. Perhaps the defining quality of any cyclical recession is the inventory liquidations. Like clockwork, you can nearly define a business cycle by the behavior of inventory. For what were surely all the wrong reasons (listening to Janet Yellen), inventory levels surged in 2014 anticipated the economy that was “supposed to be.” The “rising dollar” turmoil of 2015 pointed out the error, and US businesses finally started reducing their inventory buildup. It wasn’t, however, until Q2 2016 that the GDP estimate for inventory was negative in its outright change (as well as the second derivative that is part of the official calculation).

Leave A Comment