This week, CNBC’s Kelly Evans interviewed one of the most well-respected billionaire hedge fund managers in history, Julian Robertson. The co-founder of Tiger Management discussed global central bank collusion to depress interest rates and the subsequent creation of a bubble. “A bubble in the stock market?” the journalist clarified. Robertson replied, “Yes, ma’am.”

Billionaires from the investing world do not sport perfect track records. Nevertheless, when the .0001% speak, investors should take notice.

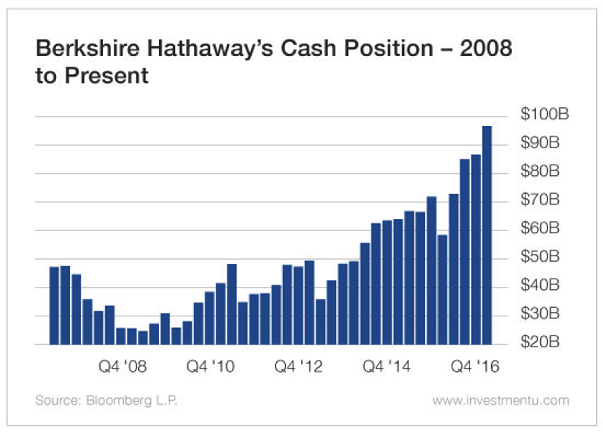

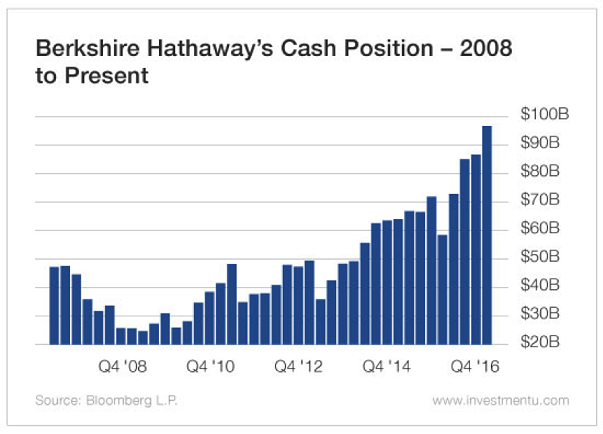

Within the past few months, the list of billionaire bull market dissenters has continued to grow. George Soros has been selling stocks throughout the summer in favor of gold. Jeffrey Gundlach suggested that investors begin “moving toward the exits.” Howard Marks warned that buying into concepts regardless of price (e.g., ‘FAANG,’ Canadian real estate, etc.) is the “…absolute hallmark of a bubble.” And while Warren Buffett preaches the virtues of buy-n-hold, his active raising of cash aligns with his desire to sell higher when others are greedy.

Most rear-view mirror thinkers concur that the dot-com collapse of 2000 represented stock market insanity. In fact, after the Nasdaq 100 lost 80% of its value and the S&P 500 plummeted 50% from its peak, people acknowledged having suffered through the bursting of a stock market ‘bubble.’

Leading into the turn-of-the-century, however, few spoke about extreme valuations in terms of eventual disaster. On the contrary. The New Economy represented a supercharged shift in technology that ‘justified’ ridiculous prices for questionable profits and modest sales.

Here in September of 2017, the masses are once again disregarding the dozen or more traditional metrics of extraordinary overvaluation, justifying them on a simplistic ultra-low-rate criterion. Although most of those metrics (e.g., market cap-to GDP, earnings, book, Q ratio, etc.) may still place 2000 as the most overblown balloon in history, the fact that 2017 comes in second place should hardly serve as solace. Indeed, to the extent revenue matters, investors currently pay the highest S&P 500 price-to-sales ratio and highest median price-to-sales ratio in history.

Leave A Comment