from the International Monetary Fund

— this post authored by Robin Koepke

A key question facing global investors today is what impact the US Federal Reserve’s monetary policy normalization process will have on capital flows to emerging markets. The IMF’s new model estimates show that normalization – raising the policy interest rate and shrinking the balance sheet – will likely reduce portfolio inflows by about $70 billion over the next two years, which compares with average annual inflows of $240 billion since 2010.

Shrinkage in the Fed’s $4.5 trillion balance sheet, which began in October, accounts for most of the impact on portfolio flows – defined as foreign purchases of emerging market stocks and bonds. Reduced availability of foreign capital could make it more challenging for emerging market economies to finance their deficits and roll over maturing debt. That is why the Fed should move gradually and communicate its plans clearly.

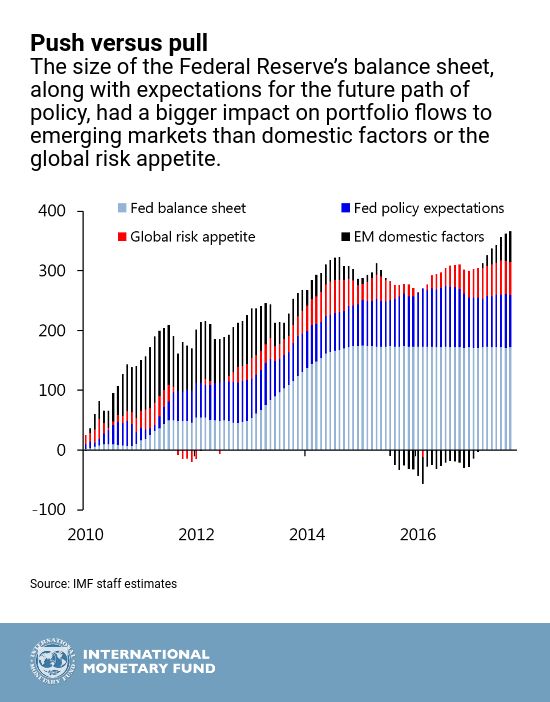

The IMF’s latest Global Financial Stability Report shows that large-scale monetary accommodation has underpinned a significant portion of portfolio flows to emerging market economies since the global financial crisis. In particular, we estimate that about $260 billion in portfolio inflows since 2010 resulted from the “push” of unconventional monetary policy by the Federal Reserve, as opposed to domestic “pull” factors. The estimates are based on an econometric model adapted from a 2014 paper. The Fed’s large scale asset purchases, which $170 billion of the total as investors rebalanced portfolios toward higher-yielding emerging market assets. Downward shifts in market expectations for future Fed policy rates accounted for the remaining $90 billion.

Our model results suggest that Fed monetary policy will continue to weigh on portfolio flows. We estimate that the reduction in the size of the Fed’s balance sheet will cut flows by $55 billion over the next two years. Flows could fall by an additional $15 billion if short-term interest rates were to rise in line with IMF forecasts. Our estimates assume that the US policy rate will rise to just under 3 percent by the end of 2019, and that the tightening process will be orderly and will not take a toll on emerging market growth.

Leave A Comment