Speculators have not been this bullish on the euro since at least 2008.

In the previous week, speculators pushed net long contracts on the euro to a new high for 2017 and now net long positioning by speculators on the euro are at a new high since at least 2008.

Source: Oanda’s CFTC’s Commitments of Traders

These charts reveal a distinct sentiment shift on the euro this year. Since 2008, speculators spent the majority of the time as firm euro bears. The new high in net long positioning going into 2018 signals strong odds for fresh momentum for the euro.

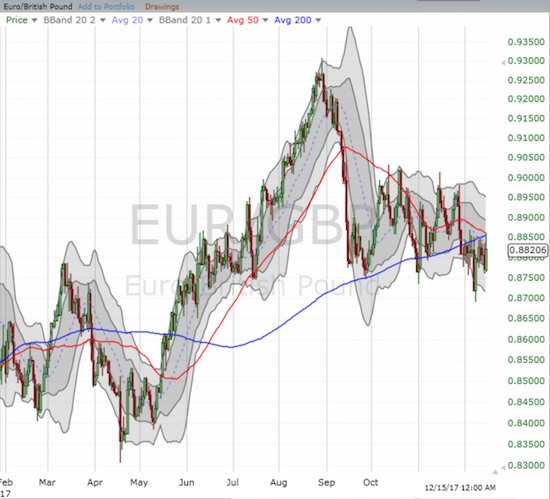

Right now, EUR/USD is pivoting around its 50-day moving average (DMA) after leaving behind a near 4-year high in September. EUR/GBP flirts with a major breakdown as it churns below converged 50 and 200DMA resistance.

EUR/USD carried a lot of momentum going away from the French elections. That momentum hit a way three months ago.

Source: FreeStockCharts.com

EUR/GBP hit a sharp peak in August. The current churn is barely staving off a major technical breakdown.

The speculative breakout in the euro came ahead of the Thursday, December 14 meeting of the European Central Bank (ECB). The euro rallied going into the meeting and sold off after the meeting and into the end of the week. I think the selling was overdone; likely a reaction to the ECB sticking to its plans for monetary policy with a general lack of strengthening in the inflation outlook. In particular, ECB President Mario Draghi reiterated that the bond purchase timeline remained open-ended. Still, I was encouraged by the ECB’s increasing bullishness on the economy. The ECB even raised its growth forecasts and noted the strengthening of the economic expansion. From the transcript (emphasis mine):

“The latest data and survey results point to solid and broad-based growth momentum…

This assessment is broadly reflected in the December 2017 Eurosystem staff macroeconomic projections for the euro area. These projections foresee annual real GDP increasing by 2.4% in 2017, 2.3% in 2018, 1.9% in 2019 and 1.7% in 2020. Compared with the September 2017 ECB staff macroeconomic projections, the outlook for real GDP growth has been revised up substantially.”

Leave A Comment