The most significant thing I’m seeing this week is my measures of risk strengthening amid large range days and high volatility. Market participants are getting comfortable with wide swings in their portfolios. The improvement in my measures of risk still aren’t enough to clear my market risk indicator, but a continued rally next week just might do it.

On the other hand, my measures of stock market quality, trend, and strength all fell this week even with four days of rally. This action is similar to what I was seeing a few weeks ago that indicate we’re probably seeing another dead cat bounce. Last week I said that I intended to take some profit from the hedge if the market retested the August low. I didn’t do it for a couple of reasons. The major reason is that at the lows on Monday the hedged portfolios were roughly allocated still at 50% long, 33% aggressively hedged (with mid term volatility), 17% short the S&P 500 Index. As a result, I would have only softened the hedge by selling some volatility and buying a SPX short. I prefer to actually get more long when the market is making a low. The second reason was the tepid response from my core indicators since the Monday low. I’m continuing to be patient and waiting for either my market risk indicator to clear or a break lower before changing any allocations.

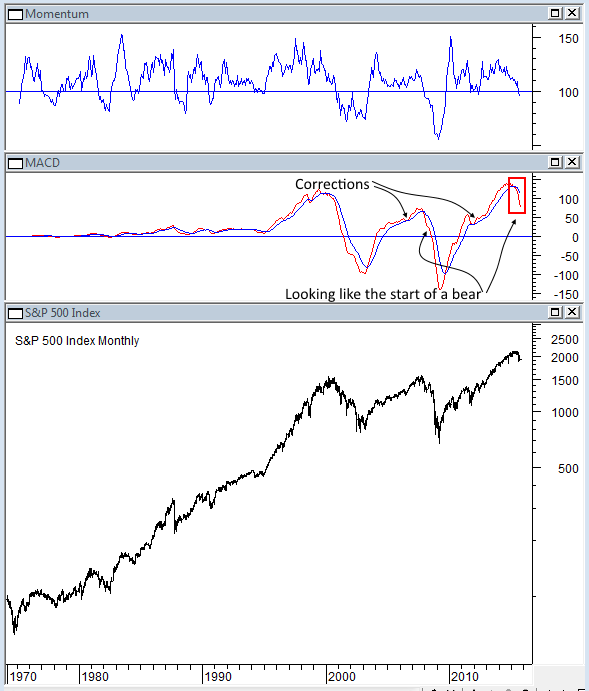

One thing of interest is that long term momentum is starting to paint a clear picture of the start of a bear market. Notice the difference between corrections that take small dips to bear markets that have MACD and momentum plunging.

Conclusion

Market participants are getting comfortable with volatility, but core indicators aren’t improving. I’ll be exercising patience while I wait for my market risk indicator to clear or price to plunge lower. Either of those events will have me adding long exposure to the hedged portfolios.

Leave A Comment