Global markets traded near all-time highs on Tuesday, with S&P futures, Asian shares and European stocks all flat this morning, while oil continued to gain on Kurdish geopolitical concerns while most industrial metals fell. The euro extended its recent slide and stocks drifted as Spain’s escalating hard-line response to the Catalonian secession threat fueled concern the crisis may intensify.

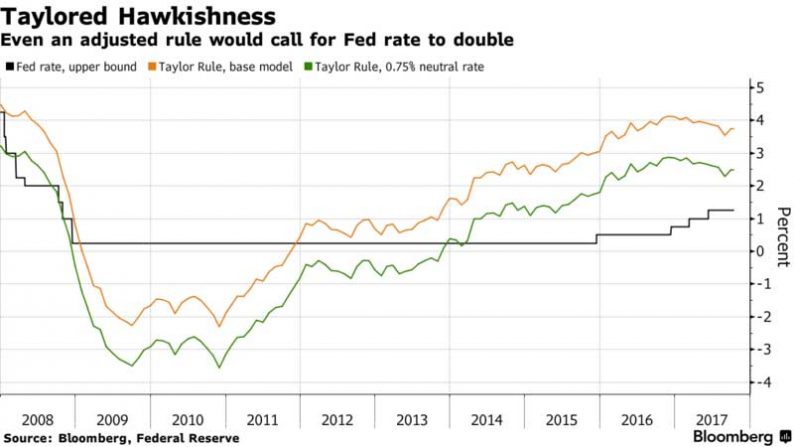

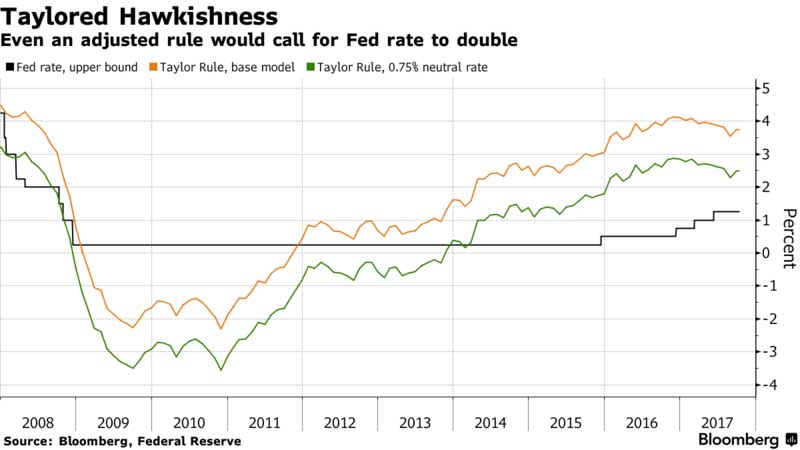

Markets initially followed the US reaction to reports of a positive John Taylor (Rule) – Donald Trump meeting, which sent 2Y Treasury yields to their highest since 2008 and pushed up the dollar higher amid speculation the next Federal Reserve chairman will be more hawkish, while TSYs briefly traded through Monday’s session lows because as we showed yesterday, the Taylor Rule would suggest a Fed Funds rate that is far higher than the current.

However, the pop in short-yields was not matched at the long end and the 2-to-10 year U.S. yield curve hit its shallowest in more than a year.

“Fed chairs have often influenced U.S. monetary policy quite considerably in the past. And I would certainly see Taylor as a candidate who would fit in this pattern,” Commerzbank analyst Thu Lan Nguyen said. “That makes one thing clear: should Trump nominate Taylor as Yellen’s successor the U.S. dollar would initially appreciate notably.”

Cable remained volatile through U.K. inflation data and dovish commentary from BOE’s Ramsden but eventually traded flat. In addition to Spain, the EUR/USD continued its recent trend lower, pricing a nine-month QE extension within ECB taper, while bunds and other EGBs continue to grind higher. The South African rand weakened following a Zuma cabinet reshuffle

The common currency declined for a fourth day, the longest streak since May. The Stoxx Europe 600 Index was little changed following mixed trading in Asian stocks earlier, after North Korea warned that a nuclear war could “break out any moment.” Core European equity markets dipped from the open before trading back to unchanged with the tech sector supported by Infineon (2.5%) after positive comments from BofA, leisure sector underperforms after Merlin Entertainments (-19.5%) posts poor earnings forecast. Spain’s IBEX Index fell 0.3 percent to the lowest in a week as Spain cut its economic growth forecast for 2018, acknowledging the impact of an escalating political crisis that led the National Court in Madrid to jail two leading Catalan separatists. As reported on Monday, the Spanish state is turning up the pressure on the separatist leaders as Prime Minister Mariano Rajoy tries to persuade Catalan President Carles Puigdemont to drop his push for independence or see Madrid take direct control of the regionl two Catalan independence leaders were ordered jailed without bail during a sedition trial.

Asia’s regional stock benchmark was little changed, holding near its highest level in 10 years, while a gauge of mining stocks advanced after Rio Tinto Group signaled it’s on track for record annual iron ore shipments. The MSCI Asia Pacific Index added less than 0.1 percent to 167.82 as of 11:40 a.m. in Hong Kong, after extending gains from its highest level since November 2007 on Monday. Materials stocks led gains Tuesday, rising 0.5 percent. Japan’s Topix fluctuated, erasing early gains, after a six-day rally pushed it further into technically overbought levels. It eventually closed 0.2% higher in Tokyo after gaining as much as 0.6%. Australia’s S&P/ASX 200 Index rose 0.7 percent and South Korea’s Kospi index was up 0.2 percent.

“Investors are pausing just a bit while waiting for more directional data points on the global state of affairs before they assess whether current high valuations have firm footing,” said Attila Vajda, managing director of Project Asia Research & Consulting Pte. China’s GDP report due on October 19 will help determine investment decisions.

Elsewhere, the pound dropped amid speculation the Bank of England will deliver the U.K.’s first rate increase in more than a decade next month after data showed inflation in U.K. accelerated in September, although testimony by Governor Mark Carney befire lawmakers in London appears to have taken away the fizzle. British Prime Minister Theresa May and European Commission chief Jean-Claude Juncker agreed over dinner in Brussels on Monday that the pace of negotiations over Britain’s departure from the European Union should be stepped up. Some market watchers such as JP Morgan are sceptical on sterling’s outlook, recommending investors to buy euros against the British pound as “the overhang of the Brexit issue itself would constrain how much accommodation the BoE would be able to remove.”

One of Monday’s big movers, oil, consolidated a near month-high having spiked after Iraqi forces seized the oil-rich city of Kirkuk from fighters loyal to the country’s semi-autonomous Kurdish Regional Government. After months of rangebound trading during which OPEC-led supply cuts supported crude values but rising U.S. output capped markets, prices have moved up significantly this month. Brent crude oil was 5 cents higher at $57.87 a barrel by 0800 GMT, up almost a third from its mid-year levels. U.S. West Texas Intermediate (WTI) crude CLc1 was nudging up again too at $51.99. There were unconfirmed reports that Kurdish forces had shut around 350,000 barrels per day (bpd) of oil production from major fields. “The 500,000 bpd Kirkuk oilfield cluster is at risk,” Goldman Sachs said in a note to clients.

Tension between the United States and Iran is also rising, after U.S. President Donald Trump on Friday refused to certify Iran’s compliance over a nuclear deal which removed long-running sanctions. “If there (were new sanctions), we expect that several hundred thousand barrels of Iranian exports would be immediately at risk,” Goldman said. During the previous round of sanctions around 1 million bpd of oil was cut from global markets.

In currencies, the Bloomberg Dollar Spot Index gained 0.1 percent to the highest in more than a week.The euro dipped 0.3 percent to $1.1764. The British pound dropped to session lows near $1.3226. The Japanese yen climbed less than 0.05 percent to 112.15 per dollar.

Yields were little changed, with the US 10-year up one basis point to 2.31%; Germany’s 10-year yield decreased less than one basis point to 0.37 percent; Britain’s 10-year yield climbed two basis points to 1.336 percent, the biggest increase in almost two weeks.

Gold declined and most emerging-market currencies weakened alongside developing-nation stocks. WTI crude resumed its push above $52 a barrel as tensions in Iraq lingered. Treasuries edged higher as odds rose that John Taylor will replace Janet Yellen at the Fed.

Leave A Comment