The chart below shows the Citi Economic Surprise Index for the US, compared against the broader G10 index, and the Europe index.

The outperformance of US positive data surprises is stark… highlighting the dramatically non-synchornized nature of global growth.

CitiFX senior trader Andrew Grosso warned that we need to pay attention to the short-term on the US data front (with next week’s payrolls, AHE and ISM all on the agenda). He expects that the time between April and July will be pivotal for the economy in terms of data suggesting the USD could outperform in the short-term.

However, the correlation between EURUSD and the spread between EU and US economic surprises, suggests EUR strength in the short-term.

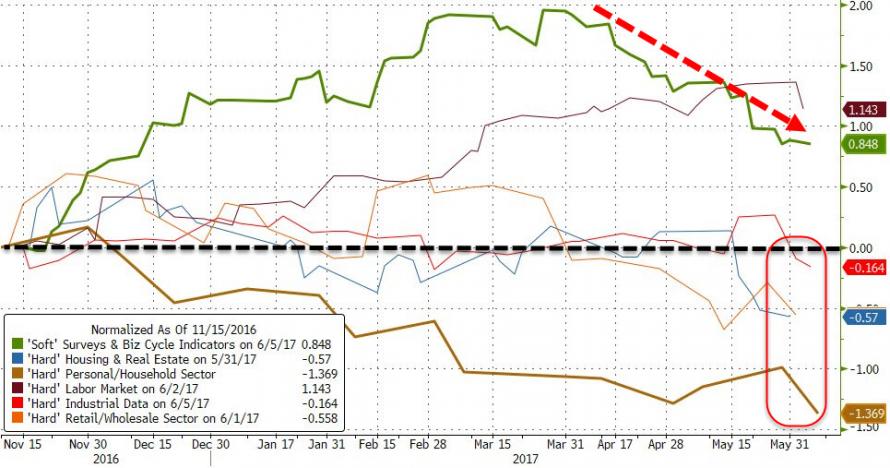

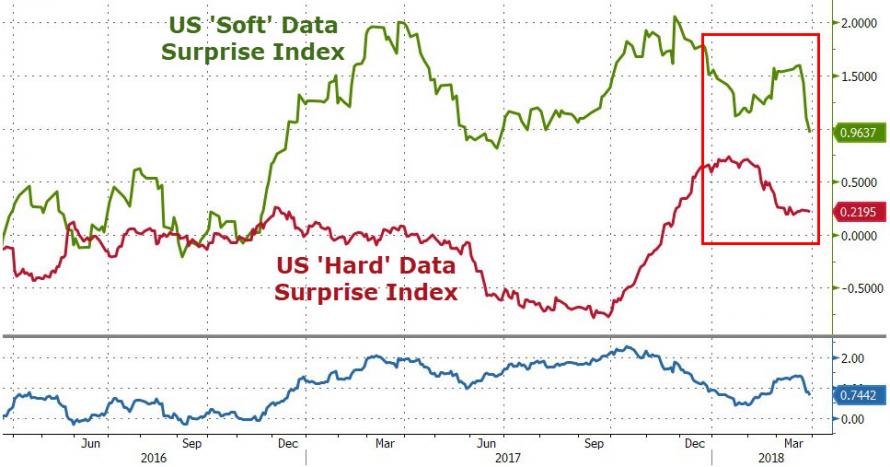

However, the relative ‘strength’ of US economic data surprises has been driven by ‘survey’ data (think ‘hope’), while all but labor are now weaker than before Trump was elected…

Or to simplify that chart…’Hard’ data is back at pre-Trump levels and now ‘soft’ survey data is crashing back to reality too…

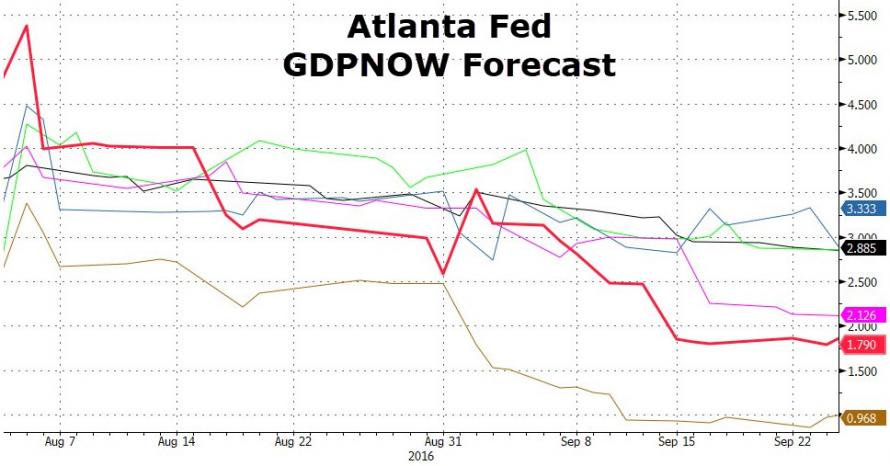

And as economic data surprises disappoint, so US economic growth expectations have collapsed…

So the question heading into Q2 is – can ‘soft’ survey-based hope keep the economic data aggregates positive enough? Or is the reflexive relationship between stocks (now falling) and expectations (now falling) gathering enough pace to spoil the party?

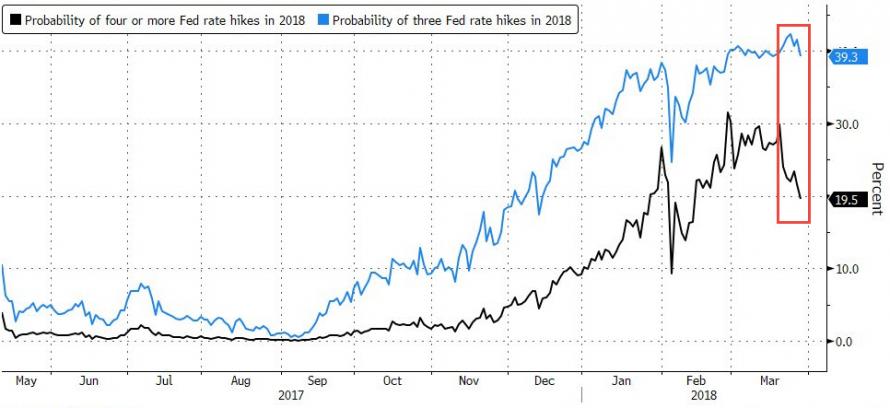

And what happens if The Fed backs away from its rate-hiking plan?

Leave A Comment