After the inflation in P/E multiples has sent the S&P 500 to to a level above the 90% percentile of all historical valuations, Goldman has called a time out, and says that there will be no more multiple expansion. As a result only one thing will push stock prices higher “as equity valuations compress as interest rates rise” – higher profits.

In his latest note, Goldman’s equity strategist David Kostin says that his tactical view remains that S&P 500 has peaked at 2400 and (unlike BofA’s recent flipflop which now expects the S&P to keep rising to 2,450 after earlier predicting a 2,300 year end target) will fade to 2300 by year-end. In fact, looking dead ahead, Goldman comes about as close as it has in recent months warning of an imminent market drop: “investors will soon capitulate on their expectation of upside to 2017 EPS forecasts as they face the reality that the accretive impact from tax reform will not occur until 2018. In fact, revisions to consensus EPS forecasts during the past few months have been negative for both 2017 and 2018.”

But don’t worry: like other recent sellside notes, any imminent corrections (or crashes) will be a “buy the dip” opportunity, and thus Goldman keeps its year-end 2019 S&P 500 target at 2500, a 6% rise from the current index level and implies a forward P/E multiple contraction of 5% to 18x.

Below are some further observations on the current state of the market from Kostin.

Thursday marked the 8th anniversary of the current bull market, making it the second-longest on record. On March 9, 2009, the S&P 500 index traded at 677 and it now stands at 2365, reflecting a price gain of 250% or 17% annualized (19% annualized with dividends). Happy Birthday indeed!

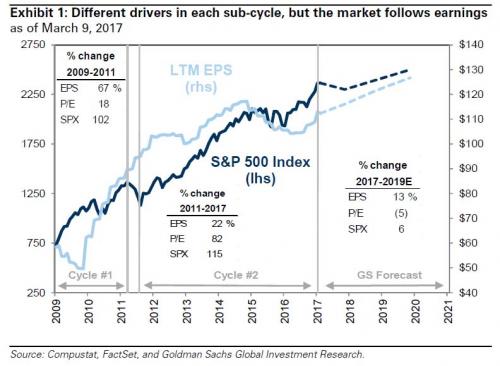

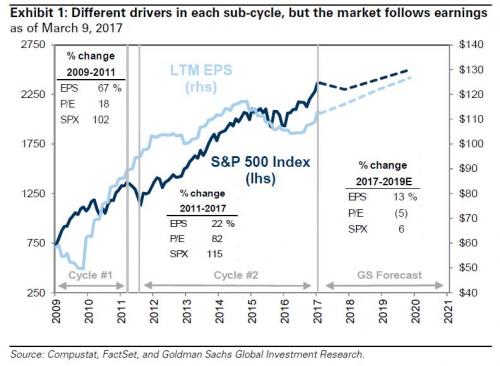

But the current bull market is really a tale of two sub-cycles (Exhibit 1).

During the first phase (March 2009 to April 2011), the market rallied on the back of a rebound in earnings from the depths of the Global Financial Crisis. Higher profits accounted for 66% of the index’s 102% gain while P/E multiple expansion explained just 17% of the rally (faster expected EPS growth contributed the remainder; see Exhibit 2).

Leave A Comment