The manufacturing soft-data reports have been nearly unanimous in reporting widespread strength that has not shown up in any hard data reports.

One exception has been Markit’s US Manufacturing PMI report that has consistently been of a muddle-through quality.

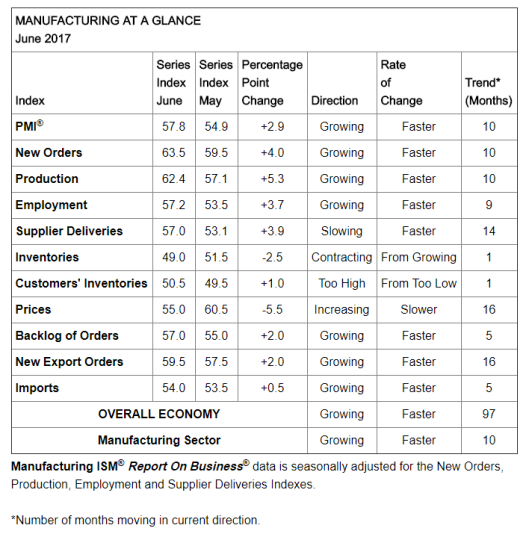

Let’s compare the ISM Report on Business to Markit’s PMI, both out today.

June ISM Manufacturing PMI

Markit PMI

Markit Manufacturing Growth Weakens Again in June

Key Findings

- Slowest rise in production volumes since September 2016

- New order growth eases for fifth month running

- Input prices broadly unchanged in June

June data pointed to a relatively subdued month for the U.S. manufacturing sector, with output, new order and employment growth all slowing since May. At the same time, survey respondents signalled resilient confidence towards the year ahead outlook, with optimism up to its strongest level since February. Meanwhile, cost pressures were the weakest recorded for 15 months, which resulted in the slowest pace of factory gate price inflation since late-2016.

Higher levels of manufacturing production have been recorded since June 2016. However, the rate of expansion was only modest and eased to a nine-month low in June. Survey respondents noted that softer new business growth continued to act as a brake on production schedules.

Some firms noted that efforts to boost inventories of finished goods helped to lift output levels. The latest rise in post-production inventories was the fastest recorded since January’s survey-record high. Stocks of purchases also increased in June, with the rate of inventory accumulation the sharpest for four months.

Chris Williamson, Markit Chief Economist Comments

Leave A Comment