While last week’s volmageddon may have subsided, its reverberations remain with many traders – certainly, the co-head of equity trading at Goldman Sachs – uncertain if last Monday’s VIX spike was a one-off event or the precursor to something far greater.

And while the events from last week are still fresh in everyone’s mind, Deutsche Bank’s derivatives team has laid out some of the most notable moves in volatility during what the German bank dubbed an “Extraordinary Week in Equity Volatility.” Here is a summary.

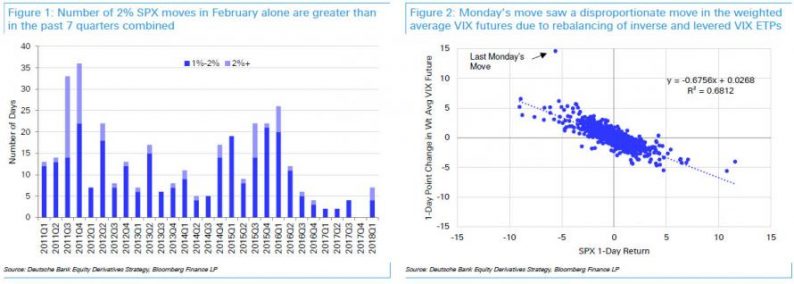

And here is the visual support of the above observations:

The number of 2% SPX moves in February alone are greater than in the past 7 quarters combined, while Monday’s move saw a disproportionate move in the weighted average VIX futures due to rebalancing of inverse and levered VIX ETPs

The volatility of VIX (vol-of-vol) hit its highest level ever as the weighted average future almost doubled over the day; at the same time SPX skew steepened considerably on Monday, the biggest one-day move in 17 years

Leave A Comment