As if defined benefit pensions funds weren’t fun enough for corporate shareholders, the Pension Benefit Guarantee Corporation (PBGC), the federal entity that backstops pension obligations when companies default, has enacted massive increases in insurance premiums for operating such plans over the past 5 years.

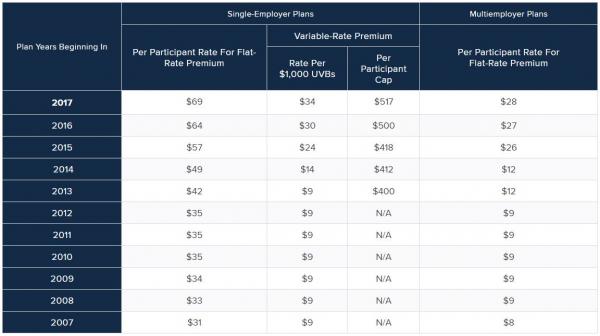

Ironically, the premiums started to skyrocket during Obama’s second term with flat-rate premiums nearly doubling from $35 per participant in 2012 to $69 per participant in 2017. Moreover, the variable rate premium paid by corporations nearly quadrupled over the same period from $9 per $1,000 of Unfunded Vested Benefits (UVBs) to $34.

Meanwhile, the rate-hike party at the PBGC is hardly over. Corporate pension operators can expect another 16% and 24% hike in flat and variable-rate premiums, respectively, over just the next two years.Which should be plenty of money to hire a bunch of new bureaucrats…

Sometimes its the taxes that aren’t necessarily called ‘taxes’ that sting the most.

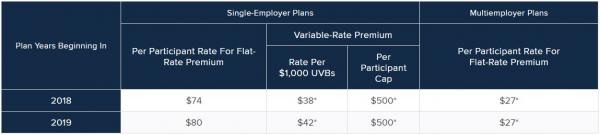

Of course, companies aren’t simply sitting back and accepting the massive ‘tax’ hikes from the PBGC. No, instead they’re crystallizing their pension debt with real debt. As the Financial Times notes, investment grade corporate debt is yielding 3.11% today which is a full point less than the 4.2% “premium” companies will have to pay the PBGC on UVB’s starting in 2019.

Companies also face a higher penalty on their unfunded pension plans from the Pension Benefit Guaranty Corporation. The premiums are based on the number of employees a company has in its defined benefit pension pool, as well as the size of its deficit. By 2019, that fee is expected to rise to 4.2 per cent, according to Bank of America Merrill Lynch.

“Only now can companies deal with the problem by issuing bonds at no incremental cost,” said Hans Mikkelsen, a strategist with the bank. “They pay the same or less to service the bonds than the insurance fees. And you know the insurance fees are going to go up.”

Yields on corporate debt remain historically low. Merrill Lynch’s broad investment grade index, shows yields averaging 3.11 per cent.

Joe Nankof, a partner at Rocaton Investment Advisors, said other companies were having the same discussions about raising debt to fund pension contributions, particularly as their deadlines to file tax returns for 2016 nears. Many companies apply for extensions to submit their returns, with that looming on September 15 for some, he said.

Leave A Comment