Northern Oil and Gas (NYSE:NOG) is familiar to long-time readers of this blog. I posted about it here, here, here and here.

I have been short this stock for some years and my view is that absent sustained high oil prices this company will file bankruptcy.

I also follow the Twitter account of Michael Reger – the company’s CEO.

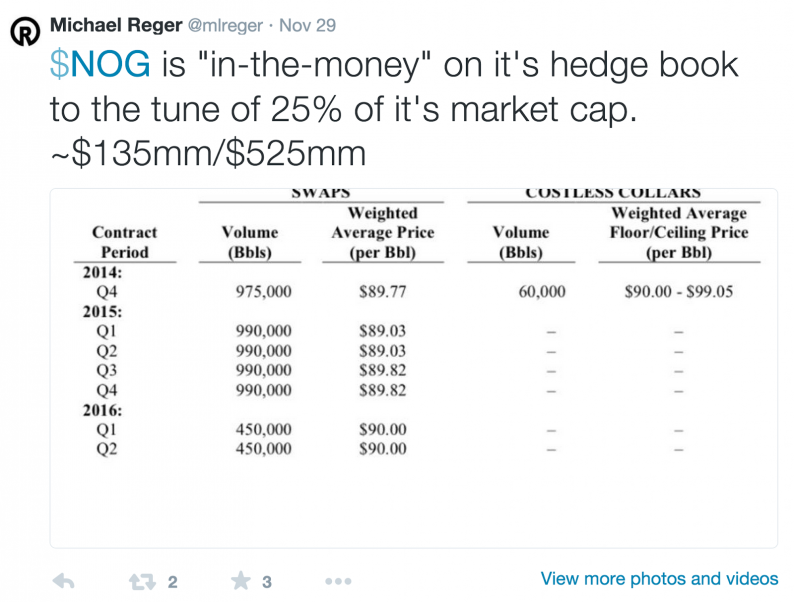

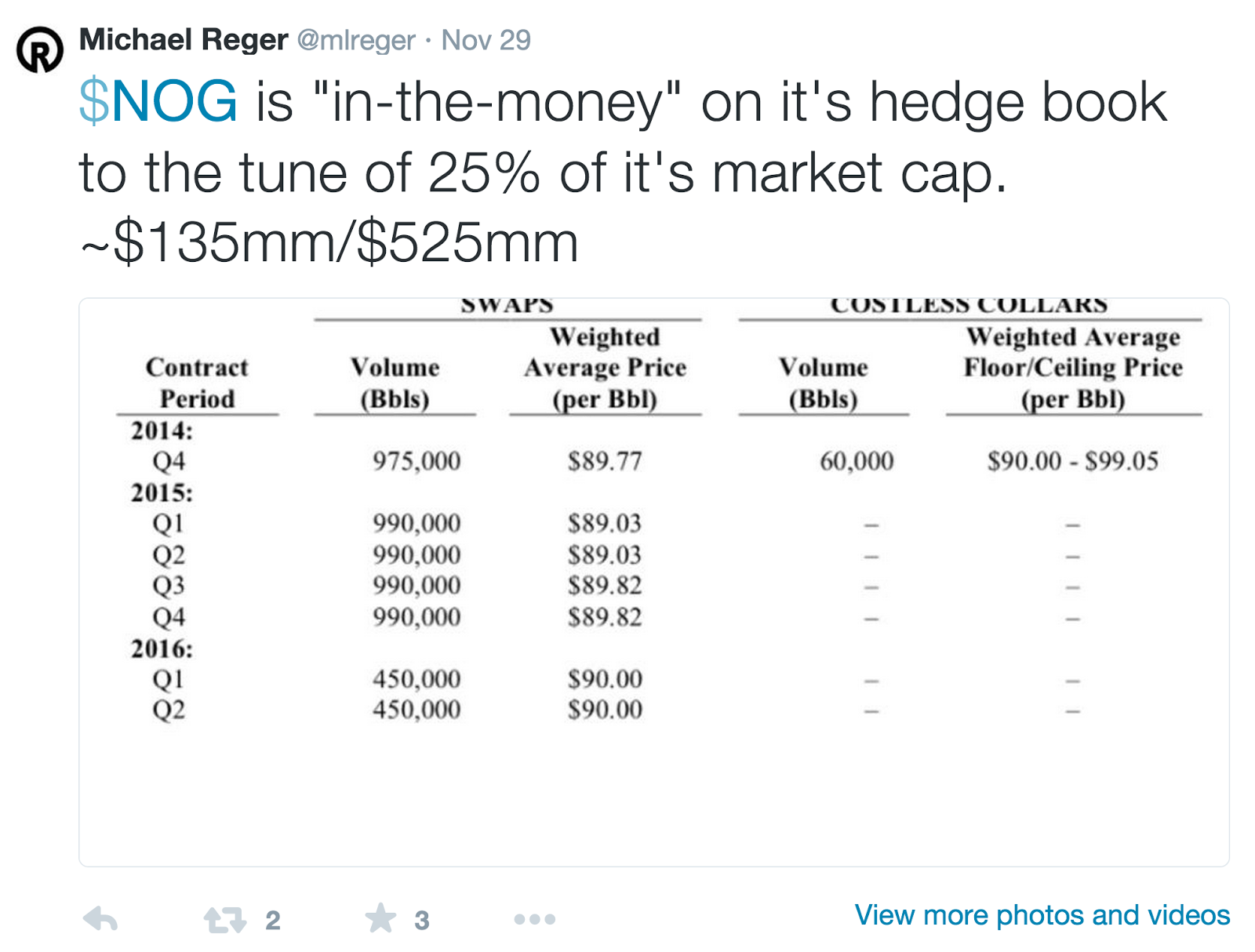

And he has been continuously retweeting this or variants on it:

In another tweet he says that “$NOG has the most capex flexibility in the Williston. Oh, and we’re hedged at ~$90.”

Let’s check this out. Northern Oil and Gas does have almost 6 million barrels of oil hedged at prices that are $20 in the money – roughly $120 million.

This is against $736 million (at last balance sheet) of long term debt. The hedges are not in the money by 25 percent of market cap – well not really – because the debt holders have first claim. The hedges are in the money by less than 20 percent of the company’s debt.

The hedges will thus repay 20 percent of the company’s debt.

The company will need to pay the rest by itself from rapidly diminishing cash flows.

Michael – please correct your tweet accordingly.

Moreover Michael pleads capital flexibility. Even that is not obvious. The debt covenants require that the company has a current ratio of 1:1. Currently the company is not close to that covenant. The shortfall (more than 120 million) likely gets subtracted from the available line.

The current ratio short-fall seems to be about the same as the hedge gains. I guess that means they can pay their current liability short fall with hedge gains…

The strange current ratio

Last quarter revenue was about $120 million. Revenue is likely to fall net of hedges.

They have current accounts payable of $220 million.

You may wonder how you possibly have accounts payable of almost twice quarterly revenue (and eight times cost of goods sold).

I will let you work that out.

Leave A Comment