Photo Credit: Mighty Travels

Priceline.com Incorporated (PCLN) Consumer Discretionary – Internet & Catalog Retail | Reports February 17, Before Market Opens

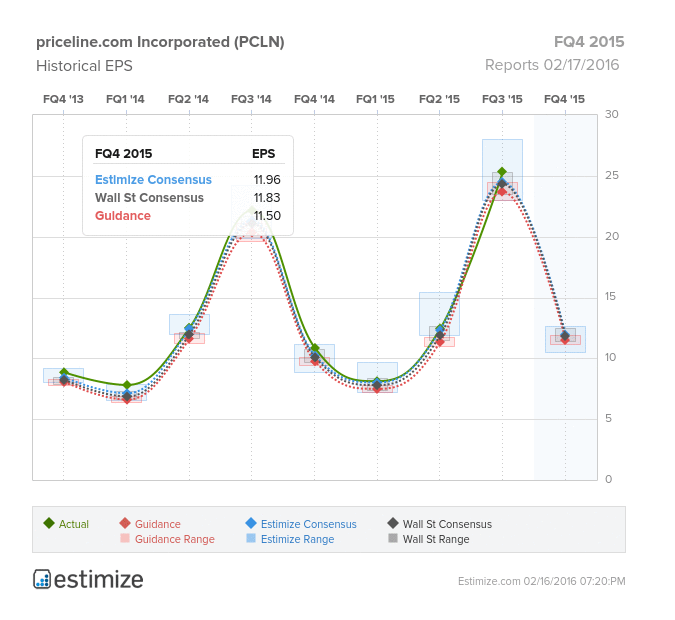

Key Takeaways

For years, online travel has been a high growth industry, but recent headwinds have come at the expense of profit growth for Priceline and its peers. Lately, though, the impact of stiffer competition, weaker conditions in China and currency headwinds have put Priceline under pressure. In the last 3 months, shares have fallen 18.5%, leading to a downgrade of its rating from buy to neutral.

Coming into Priceline’s fourth quarter earnings, investors are increasingly nervous about the company’s ability to regain its earnings potential. The Estimize consensus is calling for EPS or $11.96, 13 cents higher than Wall Street, and revenue expectations of $1.987 billion, roughly $11 million higher than the Street. Compared to Q4 2014, this represents a projected YoY increase in EPS by 11% and revenue by 8%. Priceline has consistently delivered positive earnings surprises, beating in each of the trailing four quarters. This is a company that often beats on the bottom line, surpassing the Estimize EPS estimates 94% of the time.

A substantial part of the plunge in share prices came after Priceline’s third quarter earnings, when the company delivered weak guidance about future earnings. However, nothing has changed in the business’s core strengths as Priceline continues to deliver impressive earnings despite weak economic conditions. The company’s sheer volume in available properties compared to its peers, has put Priceline in a position in which it can afford to place excess inventory on TripAdvisor’s Instant Booking platform without giving up its competitive advantage. The company’s recent partnership with Facebook and the open integration of OpenTable in its legacy platforms are expected to gain further traction.

Leave A Comment