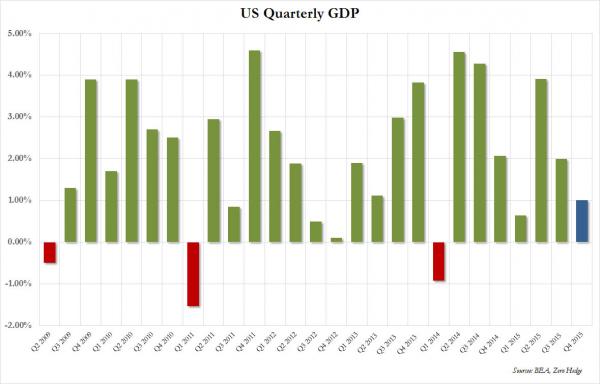

With Wall Street consensus expecting the poor first Q4 GDP estimate of 0.7% to be revised even lower to 0.4%, and with Wall Street’s biggest former permabull Joe LaVorgna expecting a number as low as 0.1%, instead it received a surprising jolt to the upside when the BEA reported that instead of a decline, Q4 GDP was actually revised higher to 1.0%.

But, as usual, the devil is in the details, because while the same consensus was expecting Personal Consumption to remain unchanged at 2.2%, instead it declined to 2.0% Q/Q, providing 1.38% of the 1.00% GDP bottom line, down from 1.46%.

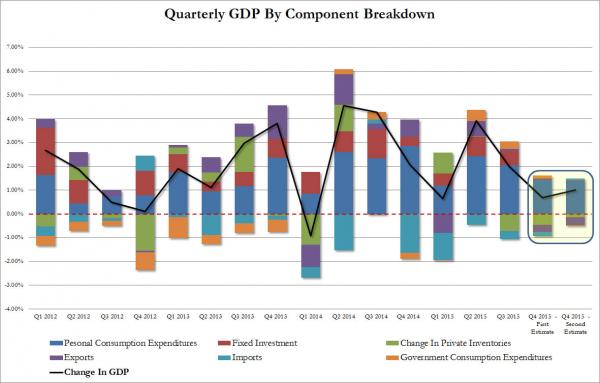

So what provided the upside kicker? The full breakdown is shown below.

In case it is not clear fromthe chart above what happened, the answer is simple: instead of the substantial, and much needed, inventory liquidation that supposedly took place in Q4 as of the last GDP estimate, when the change in private inventories declined from $95.3 billion to $75.8 billion, subtracting 0.45% from the GDP print, this number was revised much higher, to a $90.6 billion change, which subtracted just 0.14% from the print and in effect contributed +0.31% to last month’s GDP estimate, or in other words, all of the upside revision.

What this means is that while Q4 GDP was “saved” due to the lower than expected inventory decline, instead the inventory liquidation will now seep into Q1 2016 GDP and subtract from first quarter growth. Add in collapsing CapEx from the energy sector, and suddenly the weakness which was supposed to have been “kitchen sinked” in the last quarter of 2015 will be carried over to 2016.

Leave A Comment