Pre-market futures reflected the global jitters following the exogenous shock of the Russian jet shot down by Turkey near the Syrian border. The S&P 500 sold off at the open despite the 8:30 upward revision of Q3 GDP from 1.5% in the Advance Estimate to 2.1% in today’s Second Estimate. The selloff accelerated with 10AM release of the highly disappointing November Consumer Confidence report, the lowest reading in 15 months and an unwelcome bit of news at the threshold of the holiday spending season. The S&P 500 hit its -0.78% intraday low shortly after the bad Confidence report and then made a sharp reversal, trading to its 0.36% intraday high early in the final hour. The index closed with a fractional gain of 0.12%.

The yield on the 2-year note closed at 0.93%, down 1 bp from yesterday. The 10-year note also dropped 1 bp to close at 2.24%.

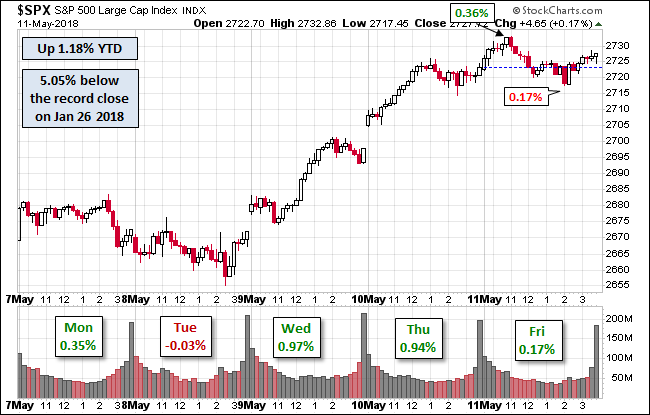

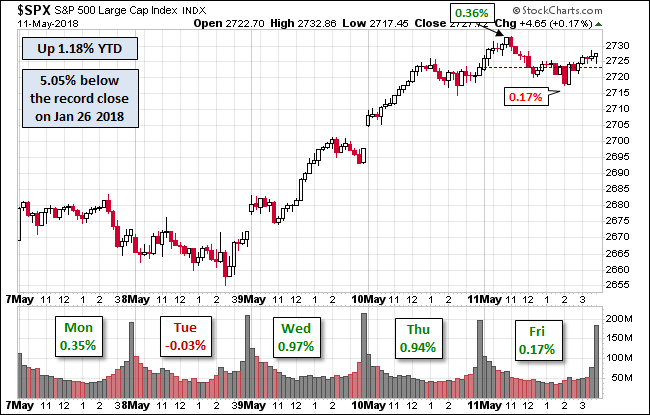

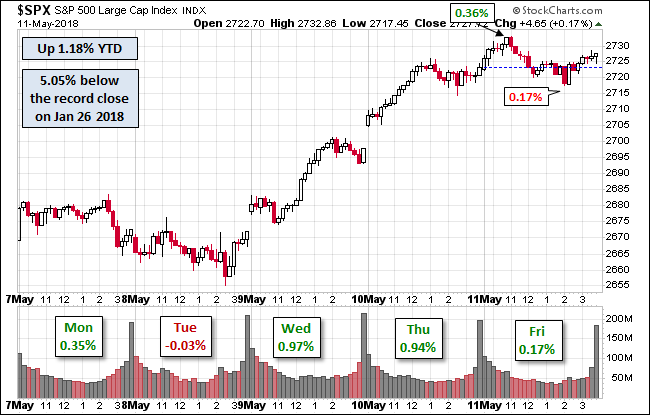

Here is a snapshot of past five sessions.

Here is a daily chart of the S&P 500. The intraday low was not far above its 200-day moving average. Volume was unremarkable.

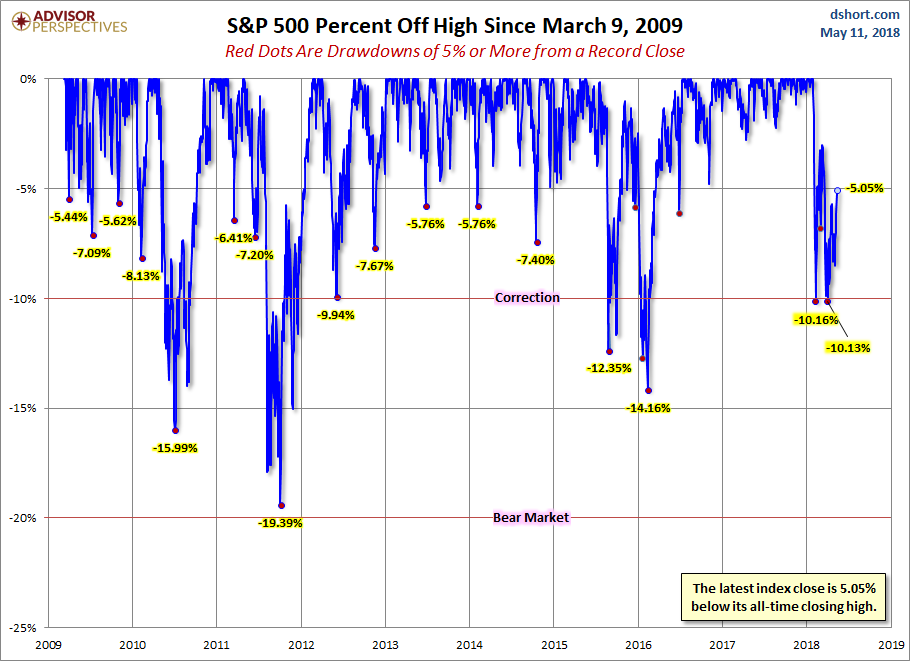

A Perspective on Drawdowns

Here’s a snapshot of selloffs since the 2009 trough.

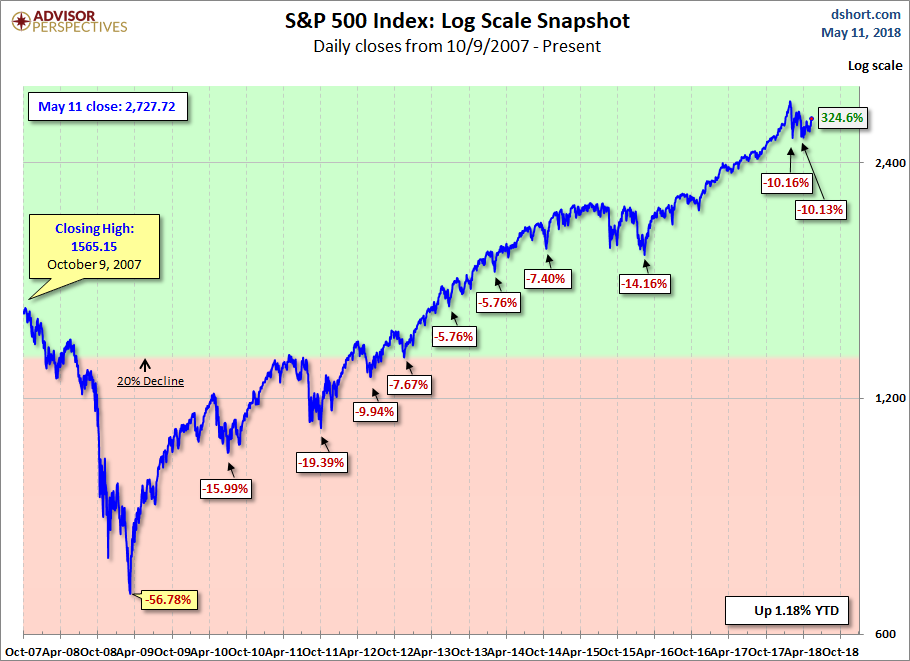

For a longer-term perspective, here is a log-scale chart base on daily closes since the all-time high prior to the Great Recession.

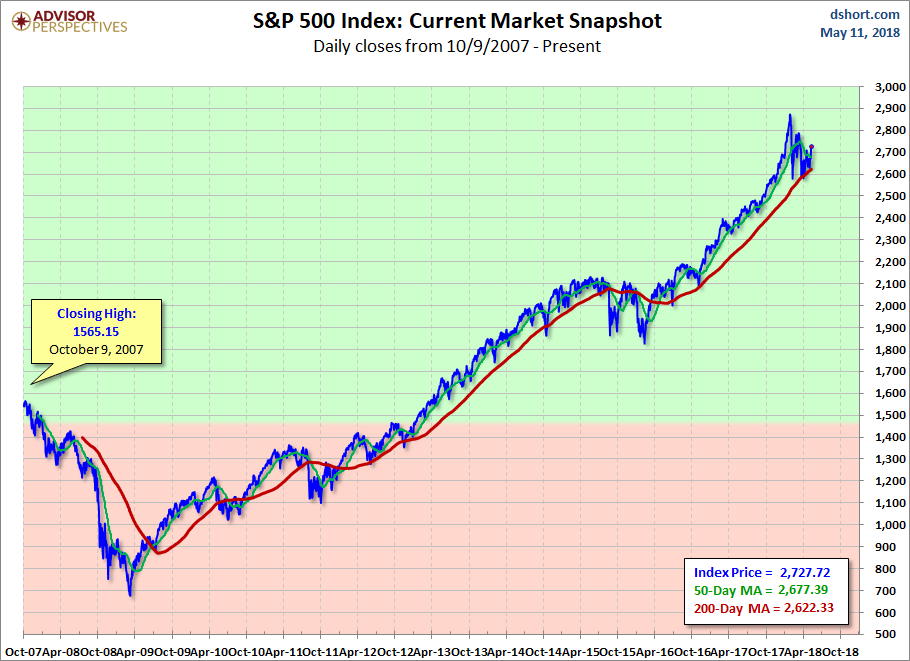

Here is the same chart with the 50- and 200-day moving averages. The 50 crossed below the 200 on August 28th.

Leave A Comment