When it comes to estimating China’s total outstanding debt, there has long been confusion about the real number with most putting the debt/GDP at around 250%, while the IIF last year calculated China’s debt load as high as 300% of GDP.

Now, China watchers can one add another ~40% of debt/GDP to the total because according to S&P, China’s local governments have accumulated 40 trillion yuan ($5.8 trillion) – or even more – in off-balance sheet debt, suggesting the already record surge in defaults is set to accelerate further.

“The potential amount of debt is an iceberg with titanic credit risks”, S&P credit analysts wrote in a report Tuesday, Bloomberg reported, with much of the build-up related to local government financing vehicles (LGFV), which don’t necessarily have the full financial backing of local governments themselves.

LGFV debt has emerged as a growing risk for China’s economy, because with the national economy slowing, and as a result of a crackdown on shadow lending and a Beijing quota for issuance of local-government bonds not enough to fund infrastructure projects to support regional growth, authorities across the country have resorted to LGFVs to raise financing, according to S&P.

That’s left LGFVs “walking a tightrope” between deleveraging and transforming their businesses into more typical state-owned enterprises, S&P warned.

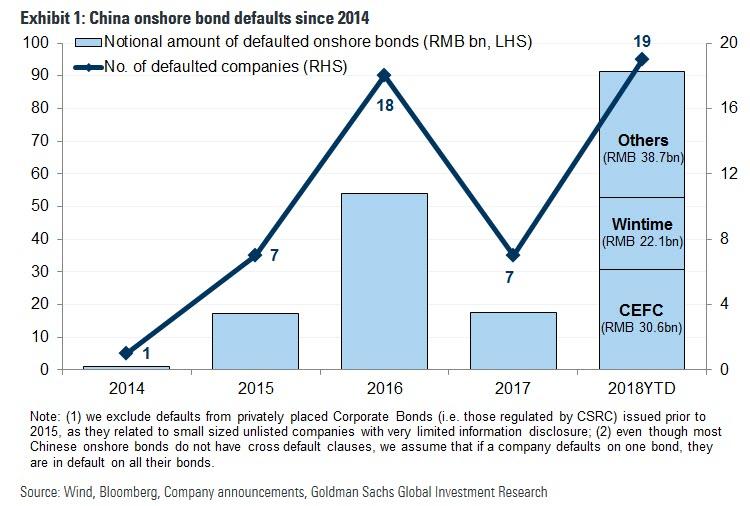

Meanwhile, debt vulnerabilities continue to rise as a result of the previously reported record surge in Chinese corporate defaults this year, as Beijing seeks to roll back a decades-old practice of implicit guarantees for debt.

And while so far LGFV debt has avoided an event of default, several issues have come close, with local government bailouts taking place only in the last minute, adding to concerns about LGFVs vulnerabilities. Meanwhile, according to S&P the riskiest LGFVs include the following:

Leave A Comment