August is lining up to be the best month for Treasury bonds in a year as 10Y Yields are down almost 13bps (the most since Aug 2017’s 18bps drop). That could be a major problem for the record amount of speculative shorts that have piled into the ‘No brainer’ bond bear positioning over the last few months…

As Jeff Gundlach warned over the weekend, Treasury bets are so extreme that they’re becoming a contrarian indicator in themselves.

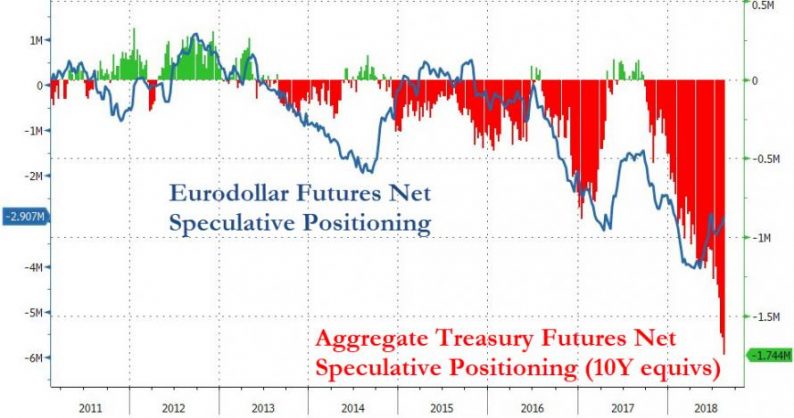

Massive increase this week in short positions against 10 &30 yr UST mkts. Highest for both in history, by far. Could cause quite a squeeze.

— Jeffrey Gundlach (@TruthGundlach) August 17, 2018

As Bloomberg notes, the 10-year short surged last week to just shy of 700,000 contracts – 70% more than the previous record set in February 2017 and it exceeds the record long set in August 2007 by about 90,000. Shorts across 2-, 5-, 10- and 30-year Treasuries are even more unbalanced at a total of 1.61 million – that’s 80% above the previous record short and more than twice as large as the peak long.

All of which is why we wonder, with 10Y Yields tumbling once again today, whether reality is dawning on the speculators that perhaps all is not well in the economy, inflation is not about to go ‘hyper’, and The Fed is not going to be able to normalize (because the economy – meaning global markets – can’t handle it)…

10Y Yields have erased all the BoJ-rumor spike losses and since topping 3.00% (“see, rate are going higher, bond bull market is over”) have plunged to one-month lows…

As we noted previously, speculators appears to be pricing in over 50bps of yield rise over current 10Y rates – as Gundlach notes, if the market gets a safe-haven jolt (cough EM crisis cough) or growth scare (cough China cough) then this massive short position might squeeze yields dramatically lower…

Leave A Comment