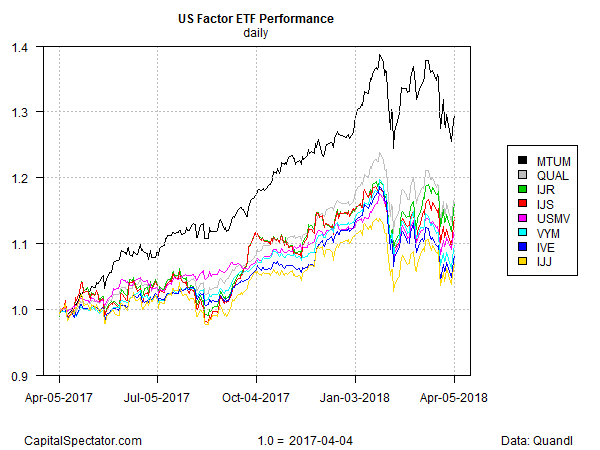

Momentum-based strategies have led the factor-investing horse race for US equities in recent history, but the latest surge in market volatility may be its undoing. For the trailing 30-day period, the momentum factor’s modest loss leaves it in last place, based on a set of ETFs tracking key US-based factor strategies. By contrast, the best-performing factor strategy for this time window – core small-cap stocks – has managed to post a modest increase.

The iShares Edge MSCI USA Momentum Factor (MTUM) is in the hole by a bit more than 3% for the trailing one-month period. On the flip side, iShares Core S&P Small-Cap (IJR) is ahead by 1.5%. The broad stock market, based on SPDR S&P 500 (SPY), is down by roughly 2% for this time period.

One month may not mean much, but it’s striking to see the momentum factor struggling in relative and absolute terms. MTUM, after all, has consistently dominated results in the equity factor space for an extended run and so the recent shift in leadership may mark a sign of things to come.

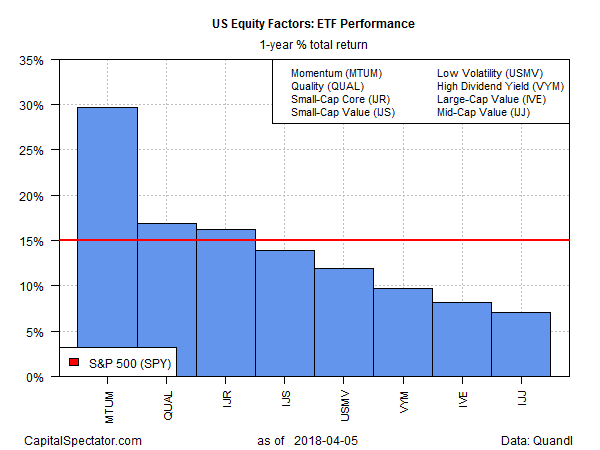

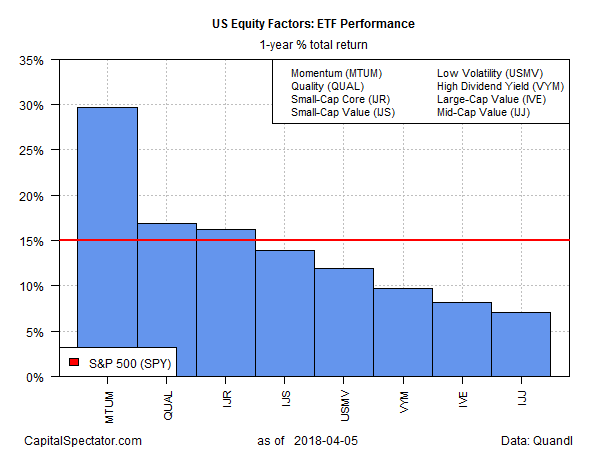

Keep in mind, however, that momentum’s upside bias is still intact for the one-year trend, providing support for thinking that the factor strategy’s dominance may still have room to run. Although returns across the board have been trimmed over the past two months, MTUM’s leadership remains unchallenged for trailing one-year returns: the ETF is up just shy of 30% as of yesterday’s close (April 5) vs. the year-ago level. That’s still a hefty premium over the rest of the field and the broad US equity market.

But as the performance chart below reminds, volatility has returned to the formerly placid terrain of factor performances. It’s unclear if MTUM’s dominance will survive the rebound in market turbulence. Based on the results for the past several weeks, there’s a new reason to wonder if the leadership lineup in the factor space is finally due for a change.

Leave A Comment