The following stock valuation is about a stock which experienced a heavy decline in its share price the past weeks due to a weaker performance in 2016 and a not so good looking outlook. It is about Target, which operates in the retail sector. A sector which will have a tough future due to a hard competition through especially Amazon. Nevertheless, Target wants to adjust their strategy by lowering prices and to stay competitive. Target is also my largest position in my portfolio and the recent drop made me think of adding more stocks. So lets see if it is worth to add more stocks of this dividend aristocrat.?

Target (TGT) is a discount retailer in North America. Target operates in three segments, U.S. Retail, U.S. Credit Card and Canadian. It offers products to customers through store locations as well as online. As of January 2012, the company operated 1763 stores and employed 365,000 people. The company was founded in 1902 as Dayton Dry Goods Company and is based in Minneapolis, Minnesota. It has increased its dividend for almost 49 years.

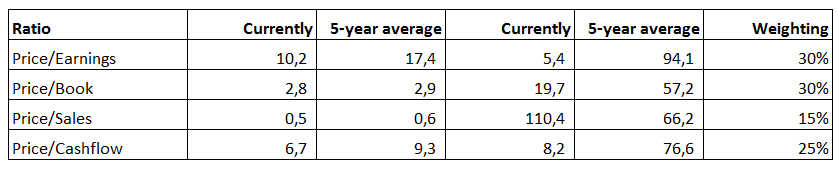

Valuation

Currently, TGT is priced at 55.17 USD per share.

If I take the weighted average of the 4 ratios according to the 5-year average the price would be at 74.48 USD. That means the current price is 25.9% below its 5-year average. The 5 year high was at 84.86 USD about 6 months ago, so currently the stock trades 34.7% below its 5-year high.

The fair market value ratio of beverage-soft drinks (consumer defensive), according to morningstar is currently at 0.95. If I divide the current price by it I will get a price of 60.37 USD.

Earnings per share growth

In 2011 the EPS were at 4.00 USD and EPS in 2016 were at 5.31 USD. This makes it an average growth per year 5.8%. Until now everything looks like the buy but considering the lower guidance in EPS of about 4 USD in 2017. The forward P/E ratio would be at 13.7, which is still below the 5-year average.

Dividend History and Future

TGT has an impressive dividend history with increasing the dividend for 49 years in a row. In the last 5 years, the average growth per year is 20.79% based on a dividend of 0.84 USD in 2011 and a current full year one of 2.16 USD. The payout ratio with 40.7% is currently still on a reasonable level, considering EPS of 4.00 USD in 2017 and a full year dividend of 2.40 USD the payout ratio will be at 59.4% also still on reasonable a level.

Leave A Comment