I’ve been building more quantitative trading models recently. I know that some hedge funds calculate the stock market’s “fair value” and then trade around that fair value. For the record, this is not what I do with the Medium-Long Term Model.

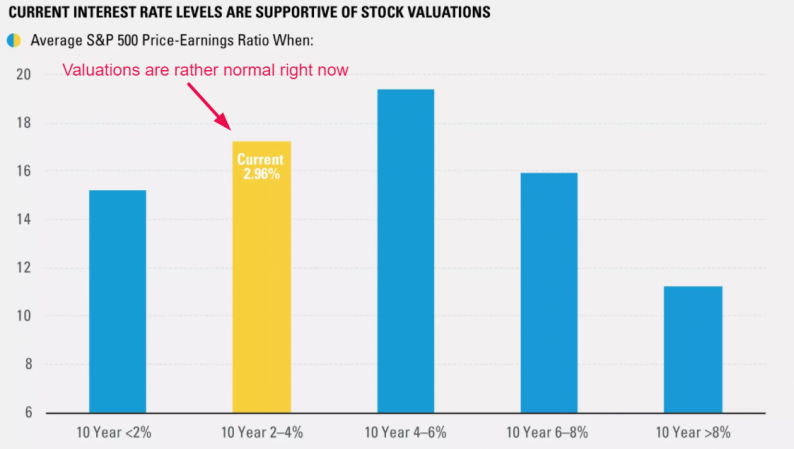

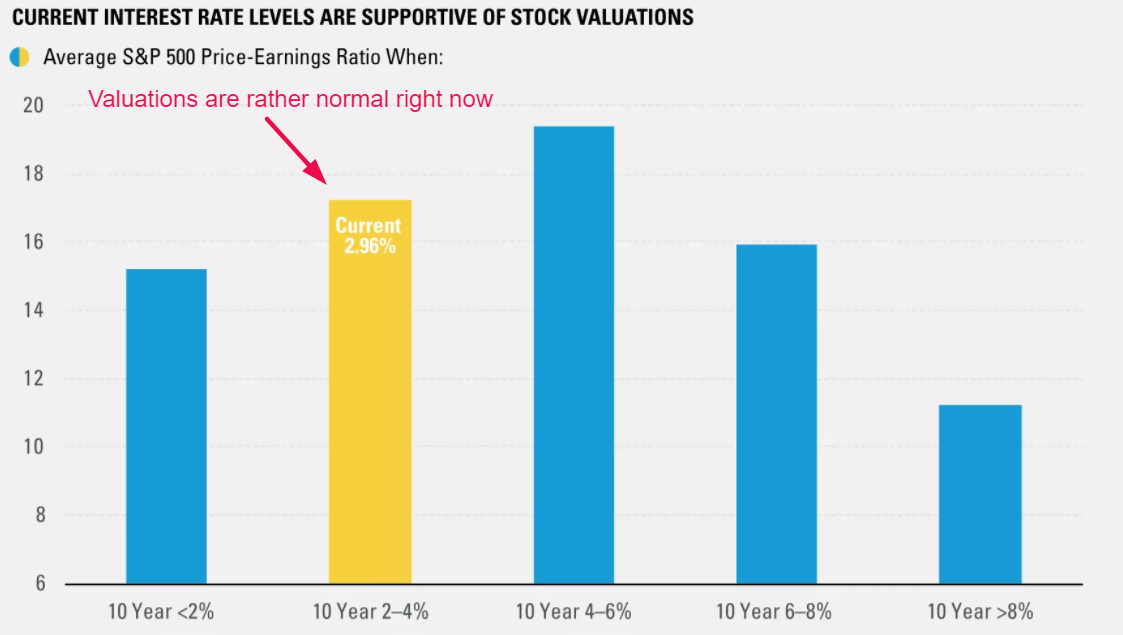

This “fair value” is usually “the stock market’s average P/E ratio during certain market environments”. Here’s an example of how the stock market’s average valuation (P/E ratio) – aka “fair value” – changes based on changes in interest rates.

Remember what I said:

The economy drives earnings, which drives the stock market. Hence, the economy leads earnings and the stock market in the long run.

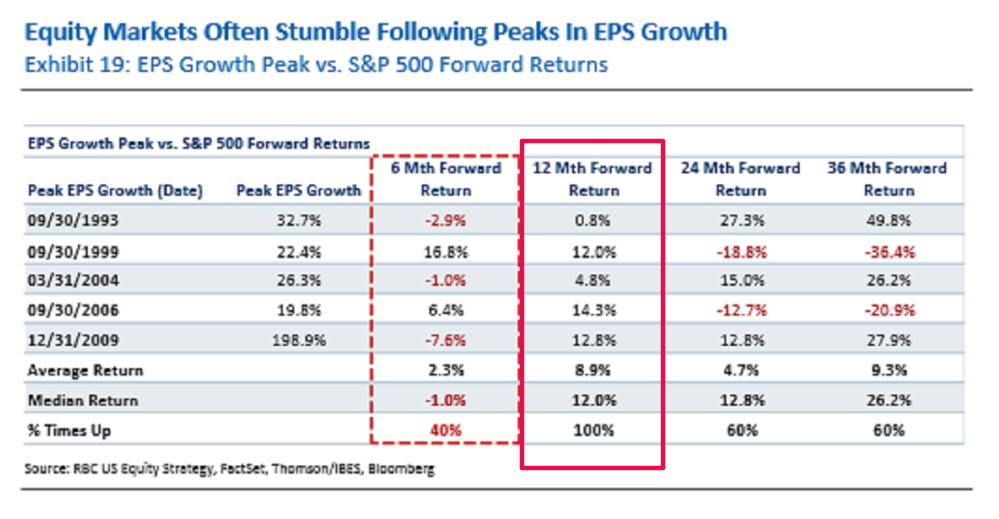

Yesterday I had a question. The economy leads the stock market. But what about earnings? Do corporate earnings lead the stock market in the long run too? This chart from April 30 demonstrated that the stock market peaks AFTER earnings growth has already peaked.

This question is especially pertinent right now. The bears are afraid of “peak earnings growth”. They think that the stock market is medium-long term bearish because earnings growth can’t possibly get better (which is true – we’ve probably hit peak earnings growth in this cycle thanks to the Trump tax cut).

But what the chart above clearly demonstrates is that the stock market does not move in sync with earnings GROWTH. Perhaps it moves in sync with earnings. My hypothesis is:

See the critical difference here? The first focuses on earnings GROWTH. The second focuses on the absolute value of corporate earnings itself.

So here’s my more important hypothesis.

Leave A Comment