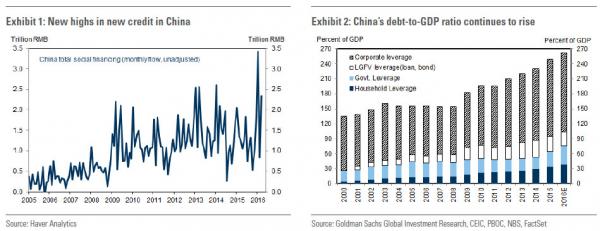

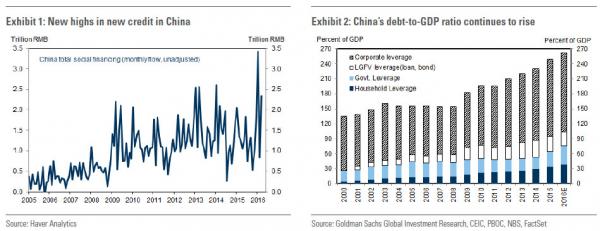

After issuing a record $1 trillion in combined bank and shadow loans in the first quarter which just like during the financial crisis provided a short-term boost to global growth (while sending China’s debt/GDP to all time highs)…

… China’s dramatic debt issuance binge is about to hit a brick wall.

According to MarketNews, Chinese bank loan growth is expected to slow sharply in April compared with March as the pillar of bank lending, mortgage loans, slowed as the property market cooled. Citing bank officials, the news service said that robust first-quarter lending almost depleted their resources, making it difficult to find good targets to lend to, which also hurt loan growth.

It also means that suddenly the credit impulse that drove both Chinese and global growth for the past two months is about to evaporate.

How big is the drop? Sources familiar with the loan number told MNI that combined new loans in April by the Big Four state-owned banks were more than halved from March’s level.As a reminder, the Big Four banks lent out CNY402 billion in March, according to the People’s Bank of China.

While there is no preview of how bit (or small) the combined TSF number will be, it is safe to assume it will be a far smaller total than the CNY2.34 trillion in total social financing that flooded the Chinese economy in March.

The slowdown mainly came from moderating mortgage growth, which has been the key driving force behind loan growth so far this year. In the city of Shanghai, mortgage loans hit a record high of CNY36.1 billion in March, beating the previous record of CNY34.6 billion set in January, according to PBOC data.

The PBOC said the country’s total outstanding mortgage loan was up 25.5% y/y at the end of March, much faster than the 14.7% of average outstanding loan growth.

But that mortgage strength in the first quarter failed to continue into April as property sales growth slowed sharply on government tightening measures. According to Essence Securities, new residential house sales in tier one cities, namely Beijing, Shanghai, Guangzhou and Shenzhen, fell 21.2% on month in April and only edged up 0.5% from a year ago, including a 38.6% m/m and 30.8% y/y plunge in the city of Shenzhen, which leads the current round of property rebound.

But if April was bad, May was a disaster: “it appears the situation is even worse into May. Shenzhen saw house sales in the first week of May plummet another 49% when compared with the previous week, dragging year-to-date sales into a 1% drop in terms of floor space.”

Leave A Comment