We live in a simulacrum society in which the fading scent of the American Dream is more a collective memory kept alive for political purposes than a reality. Even more disturbing, the difference between a phantom prosperity (or in homage to the Blade Runner film series, shall we say a replicant prosperity?) and real prosperity has been blurred by layers of simulated signals of prosperity and subtexts that are carefully designed to harken back to a long-gone authentic prosperity.

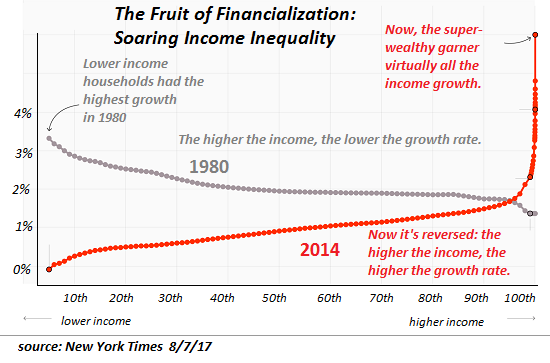

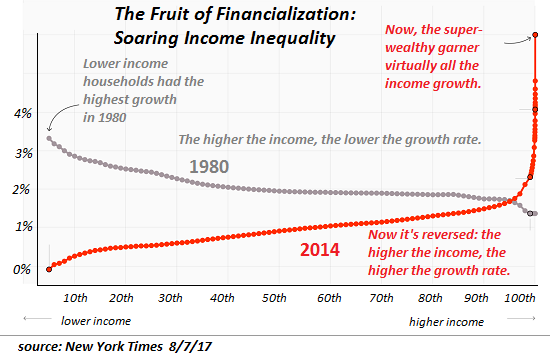

This is the reality: the American Dream is now reserved for the top 0.5%, with some phantom shreds falling to the top 5% who are tasked with generating a credible illusion of prosperity for the bottom 95%. While questions about who is a replicant and who is real become increasingly difficult to answer in the films, the question about who still has access to the American Dream is starkly answered by this disturbing chart:

If you talk to young people struggling to make ends meet and raise children, and read articles about retirees who can’t afford to retire, you can’t help but detect the fading scent of a prosperity that has steadily been lost to stagnation, under-reported inflation and soaring inequality, a substitution of illusion for reality bolstered by the systemic corruption of authentic measures of prosperity and well-being.

In other words, the American-Dream idea that life should get easier and more prosperous as the natural course of progress is still embedded in our collective memory, even though the collective reality has changed: for the bottom 95%, life is typically getting harder and less prosperous as the cost of living rises, wages are stagnant and the demands on workers increase.

Meanwhile, the asset bubbles inflated by central banks have enriched the top 10% of households, which own over 75% of all assets and take home over 50% of all household income.

“While most Americans are unprepared for retirement, rich older people are doing better than ever. Among people older than 65, the wealthiest 20 percent own virtually all of the nation’s $25 trillion in retirement accounts, according to the Economic Policy Institute.”

Leave A Comment