So another year has passed. How quickly it happened! But we hope that you did not get bored, and instead took time to learn more about the fascinating gold market. At first glance, 2017 seems to be a dull period for the yellow metal, as it was traded within a narrow range of $1,200-$1,300 for most of the year.

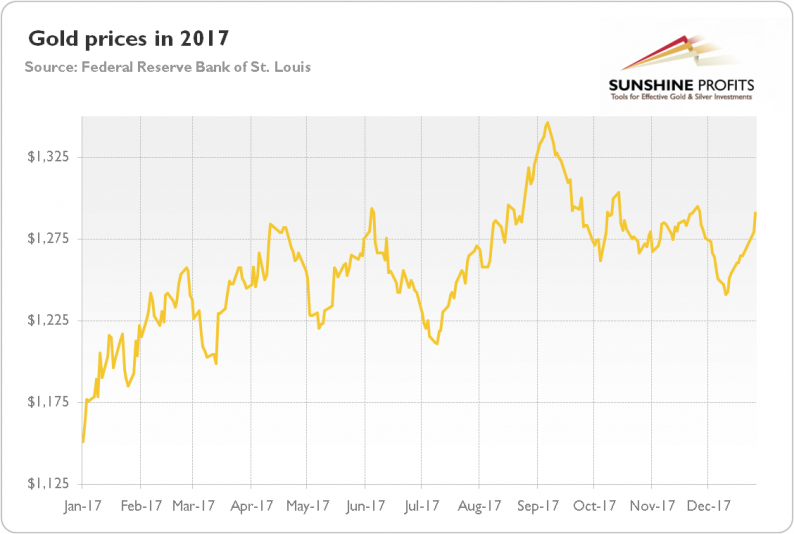

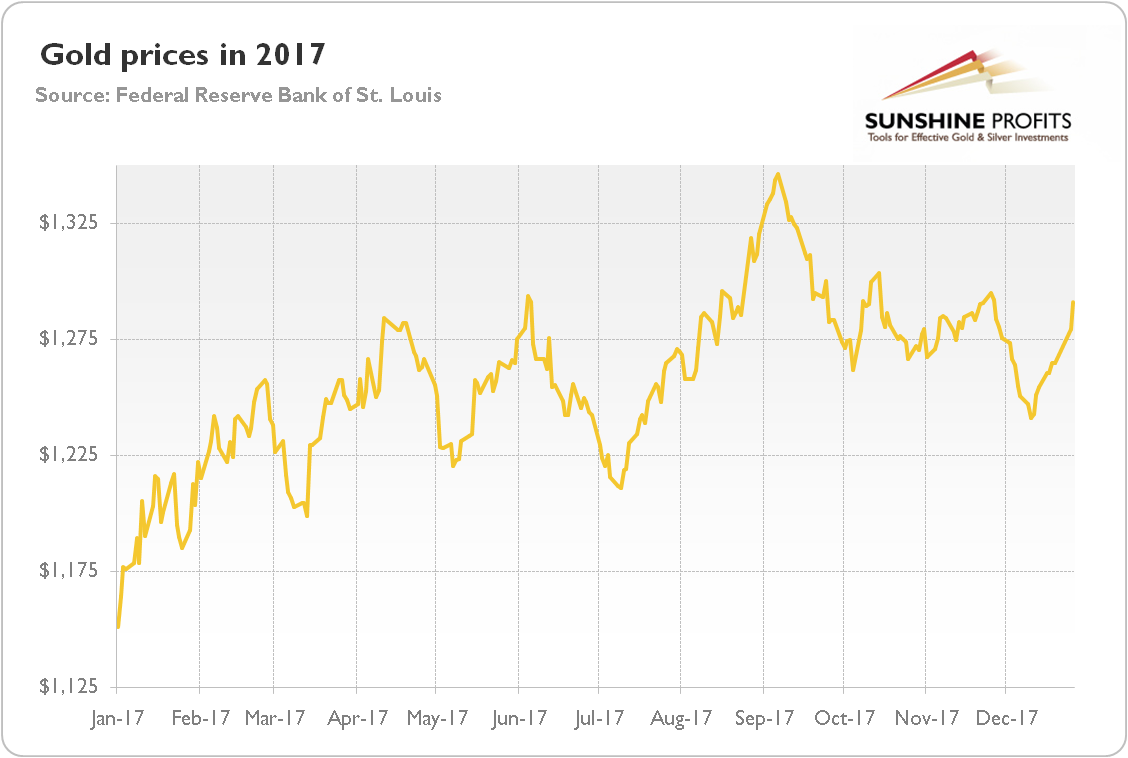

However, all that glitters is not gold, and all that does not fluctuate like Bitcoin is not uninteresting. Actually, the price of bullion gained more than 12 percent, as one can see in the chart below.

Chart 1: Gold prices (London P.M. Fix) over the last twelve months.

Surely, compared to Bitcoin’s enormous rally it is a humble performance. But we can look at this from another point of view. Gold prices rose despite the competition from the cryptocurrencies. And they increased despite, also, the Fed’s tightening cycle, subdued inflation, tightening labor markets, the stock market boom and accelerating global growth. Hence, gold’s performance is actually quite impressive given the unfavorable macroeconomic environment.

Moreover, gold gained slightly more than in 2016. And all 2017’s lows were higher than the bottoms formed in December 2016. It looks encouraging, but, on the other hand, gold failed to escape the $1,300 ceiling in a sustained manner.

As in the previous year, the first two months of 2017 were excellent for gold as the shiny metal found a bottom of only $1,132 after the FOMC meeting in December and the second interest rate hike since the Great Recession. From then, the shiny metal has been in an upward trend (although with some ups and down on the way due to the uncertainty about the North Korea, changing prospects of the U.S. tax reform or the French presidential elections, and the actions of the Fed and the ECB), reaching a peak at $1,346 in early September in the aftermath of the sixth North Korean nuclear test. Since then, the shiny metal has been in a downward trend triggered by the rebound in the risk appetite among investors (see the chart below) and in the U.S. dollar index, confirming the impact of the greenback’s value on the price of gold and the latter’s role as a safe-haven asset.

Leave A Comment