Today Macy’s dropped a bomb with results that were nothing short of abysmal, and which confirmed that not only the “legendary” U.S. spender, the driving force behind 70% of US GDP, but also foreign shoppers have hunkered down to a greater extent than at any other time during the so-called recovery.

Quickly the apologists said that this is not an indicator of overall consumer weakness as much as it is lack of retail strength: the argument being that more spending goes to online markets.

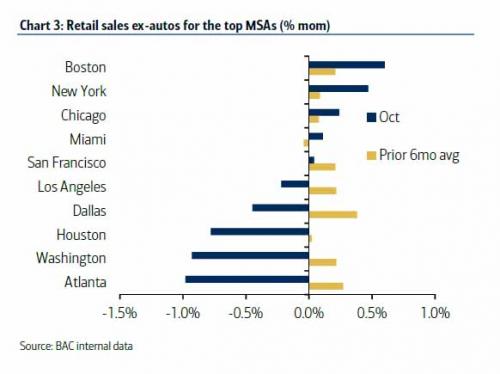

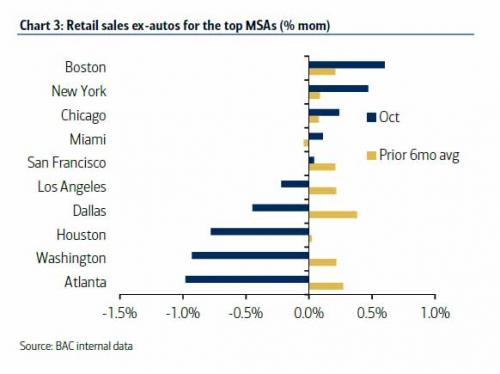

There is just one problem: if that were the case, one would see a pronounced deterioration in spendinguniformly across US cities. However, not only is that not the case, but there is a very clear distinction in which cities US consumers are doing well, versus cities in which they have been tapped out.

We know this courtesy of Bank of America’s latest credit and debit card usage data which showed a dramatic divergence among the top 10 US metro areas.

As the chart below shows, there is a very distinct slow down in spending in various cities such as Atlanta and Washington DC, both of which saw a sudden and unexpected plunge in retail sales in October compared to their prior 6 month average; sales in Houston on the other hand continue to weaken – the region has experienced essentially no growth in nominal sales over the prior six months. On the upside, the US financial centers, Boston and New York, were the strongest as one would expect.

So for those wondering where the US consumer is all spent out, look no further than the cities at the bottom of this chart.

It is not just cities, but states where the divergence is acute, but no one state has been as slammed as much as Texas. As a reminder, Texas is the first state which, due to the commodity crisis, we declared had entered a recession in April. Now, retail sales are on track to confirm this.

According to BofA, spending on BAC cards in Texas continues to weaken relative to the rest of the country. The bank adds that sales in Texas are up 1.2% yoy, down from a recent peak of 5.8% in August 2014.

Leave A Comment