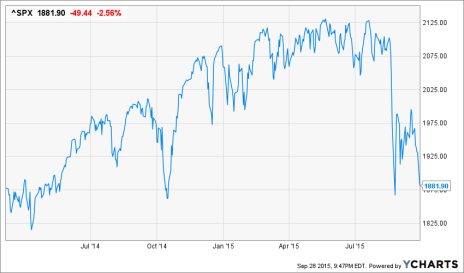

I first posted the attached three weeks ago, and here we are again, knocking on the door of the Bullard Rip low of last October 15th. While we will know soon enough whether this battered and bloodied bull will give up the ghost on this trip down and slice through 1867 on the S&P 500 or stage another half-hearted rebound, one thing cannot be gainsaid.

To wit, all the reasons for a deep correction ahead—not merely the perennial Wall Street hyped “retest”— remain in tact; and a passel of new ones have appeared, too.

In addition to the global deflation wave lapping ever closer to these purportedly decoupled shores, we now have a Fed that has decisively rendered itself into a evident state of indecision and cacophonous gibberish.

In Yellen’s case, the actual thing.

^SPX data by YCharts

In the interim, the global commodity collapse has gathered force, and is now spilling over into financial market mechanics in the form of the Glencore meltdown and CDS blowout.

Likewise, China’s supreme leader made his appearance at the White House where he professed his commitment to reform and market driven economics, and then kept the paddy wagons on the prowl for unpatriotic sellers of wholly illiquid red chips—all to no avail.

Then we have 3rd quarter earnings just around the corner. Last year’s reported GAAP reported results—the kind CEOs and CFOs file with the SEC on penalty of jail—came in at $106 per share. This means the S&P was trading at 17.6X LTM earnings.

Based on the current just-in-time markdown of the street consensus, the $97/share results reported for Q2 may slip even lower to perhaps $95 per share.

So the question recurs. Why would you now pay 19.6X earnings at the old Bullard low when it is evident that the global economy is slipping into recession and that the Red Ponzi which has artificially propelled the world economy for more than a decade is going down for the count?

Leave A Comment