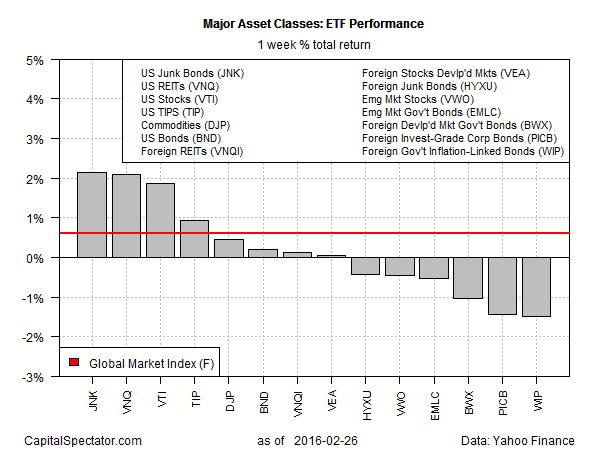

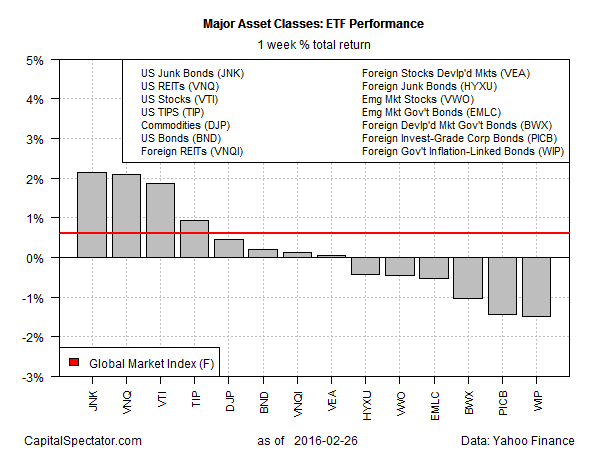

The crowd’s appetite for risky assets extended for a second week, at least in some corners, based on a set of proxy ETFs representing the major asset classes. US junk bonds took the lead for the five trading days through Feb. 26, building on the previous week’s gain. But the revival didn’t include foreign assets from a US-dollar perspective. Other than fractional gains for foreign real estate securities and equities in developed markets, all of last week’s red ink was concentrated in offshore markets via various shades of foreign bonds and emerging-market stocks.

The top winner: US junk bonds (JNK), which popped 2.1%. The week’s big loser through Feb. 26: foreign government inflation-indexed bonds (WIP), which fell 1.5%.

Last week’s upside bias for US assets was sufficient to lift an ETF-based version of the Global Market Index (GMI.F). This passively managed benchmark that holds all the major asset classes in market value weights posted its second consecutive weekly gain, rising 0.6% last week.

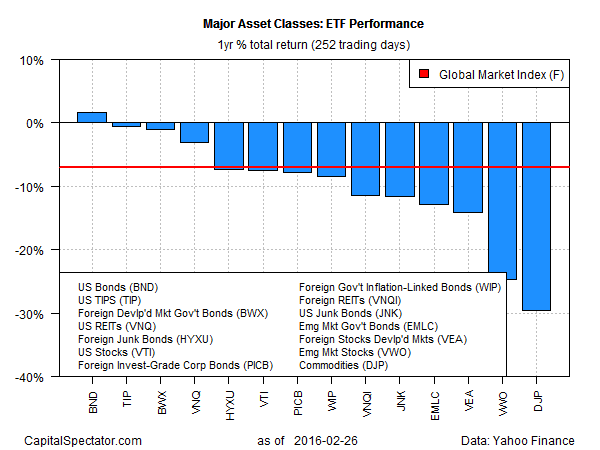

Despite the firmer pricing in recent weeks a bearish aura still weighs on most of the major asset classes for the trailing one-year period. The lone exception: US investment-grade bonds (BND), which are ahead by 1.6% for the year through Feb. 26. Otherwise, losses continue to prevail and broadly defined commodities (DJP) are still the big loser, falling nearly 30% for the trailing 252-trading-day period.

Given the negative performance winds of late, it’s no surprise to see that GMI.F continues to nurse losses for the one-year comparison. As of last week’s close, this passive benchmark of all the major asset classes is off by 7.1%.

Leave A Comment