The Fed Chorus calling for rate hikes is growing in number and intensity. In fact, there is now near-unanimous calls for a rate increase in the near future. Fed Chair Yellen all but stated that the markets should expect a rate hike in March:

Federal Reserve Chair Janet Yellen capped a week of rising expectations about an imminent interest-rate increase by explicitly supporting a hike in mid-March if U.S. economic progress persists. “At our meeting later this month, the Committee will evaluate whether employment and inflation are continuing to evolve in line with our expectations, in which case a further adjustment of the federal funds rate would likely be appropriate,” Yellen said in the text of a speech Friday at the Executives’ Club of Chicago.

San Francisco Fed President Williams – whose bank has provided key research on the current natural rate of interest – is now in the hawkish camp as is the previously dovish Brainard. NY Fed chair Dudley is on board as is Dallas President Kaplan and, Philly Fed President Harker. In short, barring a cataclysmic economic development between now mid-March, a rate hike appears a foregone conclusion.

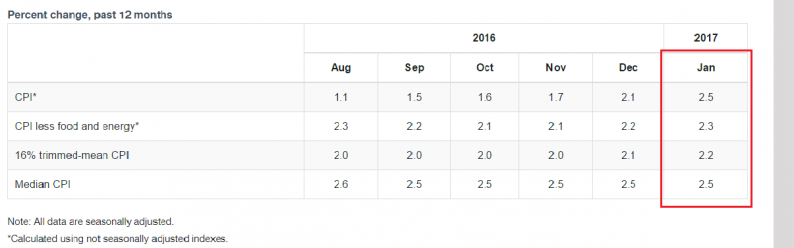

Given the strength of recent data and the current low-rate environment, it’s difficult to see any central banker not arguing for at least 1 rate hike this year. As for prices, most indexes are either slightly above the Fed’s 2% target or fast approaching that benchmark:

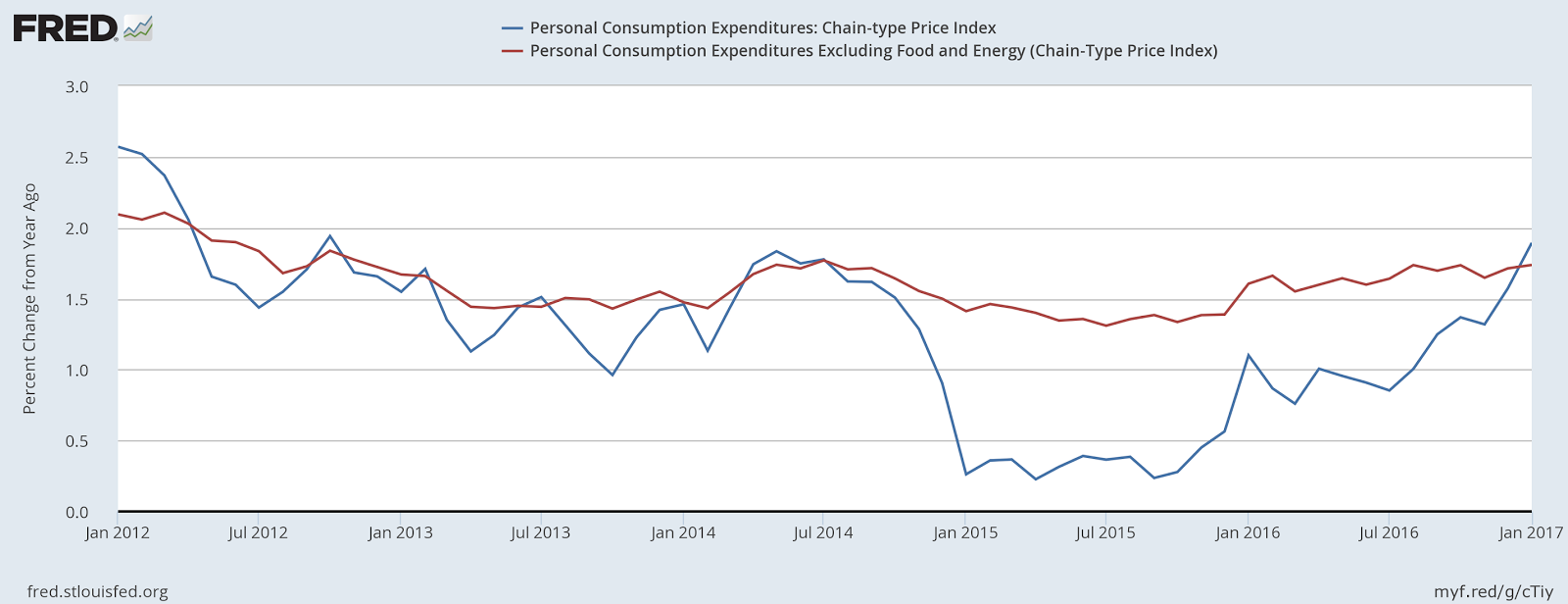

The above table is from the Cleveland Fed’s “inflation central” page; it clearly shows that the Y/Y pace of change of the BLS’s CPI gauge, along with the bank’s trimmed mean measure, are all above 2%. And Wednesday’s personal income report had PCE price indexes right below the 2% level:

The top chart shows that the core rate (in red) continues to be just below 2%. But the overall measure (in blue) shows. The bottom chart illustrates the that energy prices are the primary reason; they’re playing statistical “catch-up” after several years of dragging price indexes lower.

Leave A Comment