Fundamental Forecast for EUR/USD: Neutral

– The US Dollar was the best performing major currency last week, but gained the most ground against two currencies facing political risk, the Japanese Yen and the New Zealand Dollar.

– US Treasury yields continue to edge higher, reflecting improving growth and inflation expectations on the back of signs tax reform legislation will be passed this year.

– Retail positioning points to mixed trading conditions for the US Dollar the coming days, but positioning is tilting more and more to suggest a contrarian bullish bias.

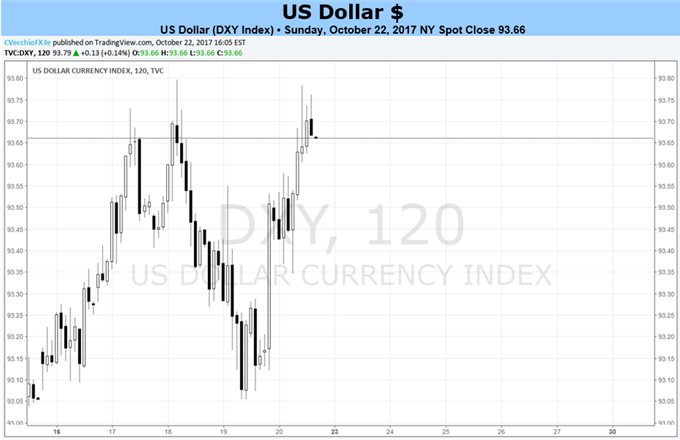

The US Dollar had a strong week, finishing at the top of the heap among the major currencies covered by DailyFX Research. EUR/USD only fell by -0.72%, but the two pairs plagued by speculation around political currents – the Japanese Yen and the New Zealand Dollar – were hit hardest. USD/JPY gained +1.50% and NZD/USD plunged by -3.04%. Additionally, with US Treasury yields continuing to march higher – the 2-year yield hits its highest level since 2008 – the greenback appears to be well-supported in the near-term.

There are some concerns that traders may want to take interest in over the coming days, however. It will be important to watch the news wires as one of the sources of recent US Dollar bullishness, the improved prospect of the US Congress passing tax reform legislation this year, still isn’t set in stone.

The coming week may also give rise to another influence: US President Trump’s pick for how will be the next Chair of the Federal Reserve. News reports, sources, prediction markets, and President Trump’s unpredictable nature suggest that it’s a coin toss between former Fed official Jerome Powell and current Fed Chair Janet Yellen.

In terms of economic data, Tuesday through Friday should capture traders’ attention. The preliminary October Markit US PMIs will be released on Tuesday, in what has collectively been a useful barometer for US growth conditions (more on that later in the week). Wednesday will bring the preliminary September Durable Goods Orders as well as New Home Sales. On Thursday both the September Advance Goods Trade Balance and the Pending Home Sales reports will be released. Finally, on Friday, the initial Q3’17 US GDP report will draw particular interest given the likely impact of the spat of hurricanes in the southeastern United States last quarter.

Leave A Comment