Economists were looking for a 2.9% rise for GDP in today’s fourth-quarter report, according to Econoday.com’s consensus forecast. The actual number, the Bureau of Economic Analysis advised, was softer than expected, decelerating to 2.6% — the slowest since the weak 1.2% gain in 2017’s Q1. The latest rise is still a decent number, although no one’s popping champagne corks over the results. On the other hand, looking through the quarterly figures suggests that the recent improvement in economic output still has upside momentum.

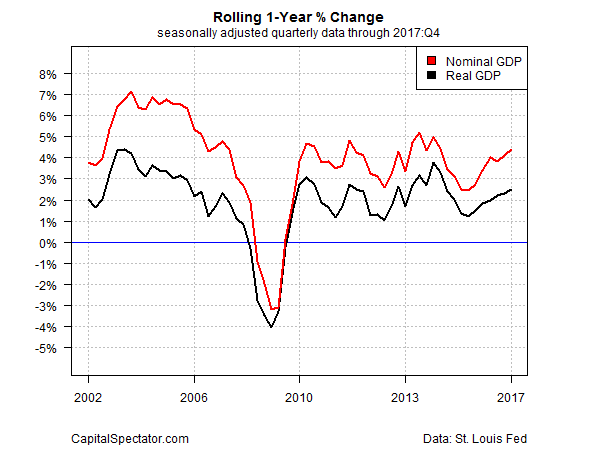

Real GDP increased 2.5% through last year’s Q4, edging above Q3’s 2.2% annual pace and touching the best year-over-year gain since mid-2015 (black line in chart below). In fact, today’s update marks the sixth straight quarterly improvement in the annual change. The year-over-year nominal change in GDP continues to improve, too.

A mid-2% trend for GDP growth is still a middling rate relative to numbers published since the recession ended in 2009. That pace also pales next to the 3%-to-4% annual gains in 2003-2006. Nonetheless, the slow-but-steady improvement in growth suggests that the economic expansion – now in its ninth year and one of the longest on record – is in no danger of ending in the immediate future. That’s also the message in this week’s profile of US business-cycle risk.

“The economy continues to hum along,” notes Ryan Sweet, an economist at Moody’s Analytics. “This is far from doom and gloom. Businesses are investing aggressively and consumers continue to spend at a very strong pace. We got a bit spoiled by 3 percent-plus growth in the last couple of quarters, but that streak was eventually going to come to an end.”

The crowd may have gotten ahead of itself recently in projecting sharply stronger growth, but the broad trend is still on the mend, extending the modest re-acceleration that began in the first half of 2016. Yet as recoveries go, the current rebound still ranks as moderate.

Leave A Comment