In a long overdue, and not exactly surprising decision, moments ago the ISDA Determination Committee decided, after punting for three days in a row, that a Failure to Pay Credit Event has occurred with respect to both the Bolivarian Republic of Venezuela as well as Petroleos de Venezuela, S.A.

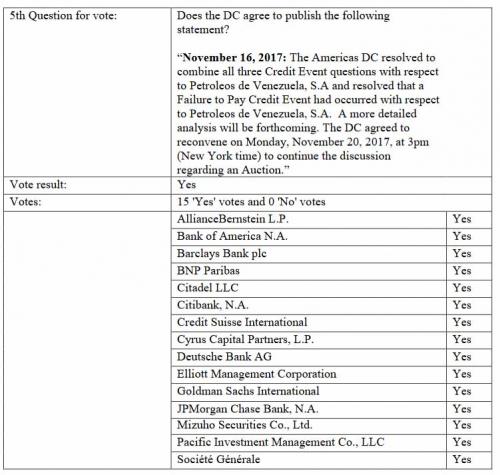

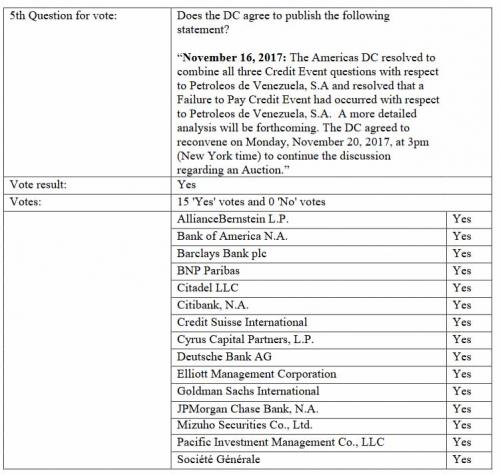

Specifically, in today’s determination, in response to the question whether a “Failure to Pay Credit Event occurred with respect to Petroleos de Venezuela, S.A.?” ISDA said that the Determinations Committee voted 15 to 0 that a failure to pay credit event had occurred with respect to PDVSA.

ISDA said the DC also voted 15 to 0 that date of credit event was Nov. 13 and that the potential failure to pay occurred on Oct. 12. ISDA also announced that the DC agreed to reconvene Nov. 20 to continue talks regarding the CDS auction, now that the Credit Default Swaps have been triggered.

Over the past week, all three rating agencies, with Fitch Ratings most recently, declared PDVSA in default, citing the state oil company’s repeated payment delays. The oil company failed to pay yet another $80 million in interest that was due in mid-October on bonds maturing in 2027, and whose buffer period expired over the weekend. Venezuela was declared in default by S&P Global ratings for a similar issue. According to Bloomberg, Fitch said that it expects PDVSA’s creditors to recover as little as 31 percent on their investment.

The panel will now meet next week to discuss whether to hold an auction to set the rate at which the CDS will pay out. When credit swaps are triggered, buyers of the contracts have their losses covered by the counterparties that sold them the insurance-like derivatives.

As recently as last month, traders had bought a net $250 million of default protection through the swaps market, according to the ISDA. Of course, with the PDVSA CDS already trading at a price which implied 100% certainty of default, none of this will be a surprise.

Leave A Comment