Some of the best long-term investments are shareholder-friendly companies that consistently reward income investors with decades of dividend growth.

These include such legends as dividend aristocrats and dividend kings, which have been raising payouts for decades in all types of economic and interest rate environments.

Let’s take a look at Wal-Mart (WMT), whose epic 44-year history of consecutive annual dividend increases makes it an aristocrat that is well on its way to achieving king status.

That being said, whether or not the stock represents a good choice for investors today, especially those looking to live off dividends during retirement, will depend on how management is able to compete with more nimble rivals such as Amazon (AMZN) in the fast-growing e-commerce space.

Business Description

Founded in 1945 in Bentonville, Arkansas, Wal-Mart is the world’s largest retailer and operates on a truly staggering scale. For example, its 2.3 million employees (1.5 million in the U.S.) serve 260 million consumers per week in 28 nations via 11,723 stores that cover 59 separate global brands.

A little over half of Wal-Mart’s stores are located in international markets, which the company entered in 1991. While Latin America, Brazil, and Mexico are important regions, the majority of Wal-Mart’s sales and profits are derived from the company’s U.S. stores (64% of revenue in fiscal year 2017) and Sam’s Club (12%).

Wal-Mart sells just about everything in its stores. Grocery (56% of U.S. sales) is Wal-Mart’s biggest merchandise category, followed by health & wellness (11%) and general merchandise (33%). Wal-Mart has its own private-label store brands, but branded merchandise still represents a significant portion of total sales. The company’s general strategy is to be the low-price leader in its categories.

In addition to its significant brick-and-mortar operations, Wal-Mart has fast-growing e-commerce websites operating in 11 countries. Walmart.com averages more than 80 million unique visitors a month and offers millions of products that can be shipped or picked up at one of Wal-Mart’s many physical locations.

E-commerce sales account for less than 5% of the company’s total revenue today but will continue growing in importance as Wal-Mart invests less in new store openings and more in its digital operations, supply chain, and logistics.

Business Analysis

Wal-Mart has done a great job of building up a wide moat in a ferociously competitive industry, one with low barriers to entry. That’s thanks to its brand recognition and omnipresence in the U.S., where 90% of Americans live within 15 minutes of one of its stores. Its stores are viewed as one-stop shops for nearly all consumer shopping needs, including groceries which account for over half of the company’s total sales.

The company’s sheer size gives it the volume and purchasing power necessary to be a genuine price leader in many merchandise categories, too. Few companies will ever be able to compete with Wal-Mart’s scale and expertise in managing supply chains and product sourcing in the brick-and-mortar space.

That being said, Wal-Mart is a classic example of a defensive mega-cap company whose large size is now working against it. That’s because the company’s enormous scale, including $487.5 billion in trailing 12-month revenue, means that moving the growth needle requires large scale, successful execution on the company’s three-year growth plan.

That plan is built around three components. First, management wants to achieve moderate 1% to 2% same-store growth in existing stores. Next, a gradual increase in global store count, such as its popular rollout of smaller “neighborhood markets” in U.S. cities, is expected to ultimately help Wal-Mart boost top line sales by $45 billion to $60 billion by the end of 2019.

Part of this plan is to reinvest into upgrading its stores to present a somewhat more upscale image. Combined with an increased focus on directing its large annual capital expenditure budget into greater employee training, especially in the use of future tech (more on this later), this has helped Wal-Mart turnaround its stagnant same-store sales figures.

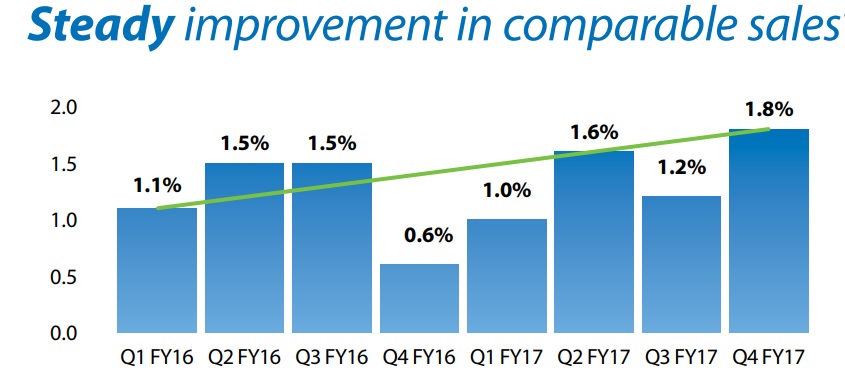

In fact, after years of steadily falling comps, the company has now generated 11 consecutive quarters of positive, if low, same-store sales growth.

Source: Wal-Mart 2017 Annual Report

Next is the company’s plan to compete with e-commerce disruptors such as Amazon (AMZN). This means fostering deeper relationships with customers to better learn their preferences and collect data that can allow Wal-Mart to further optimize its substantial supply chain.

To help with this effort, Wal-Mart spent $3.3 billion in mid-2016 to acquire Jet.com, a fast growing online retailer. Since then the company has further expanded its online empire with several more bolt-on purchases.

Source: Wal-Mart, The Motley Fool

In addition, the company is attempting to return to its upstart roots, via the creation of Wal-Mart Labs, a Silicon Valley-based division tasked with finding ways to incorporate e-commerce into its broader business model. This division recently announced Store Number 8, which according to the company “is where wild ideas, impossible notions, and big bets become scaleable realities.”

Leave A Comment