It’s a tedious time to be long emerging market assets.

Thanks to Donald Trump’s policies, the dollar is caught in a self-feeding loop that seems to tip further greenback strength one way or another. Late-cycle fiscal stimulus is buoying the U.S. economy and raising the risk of an inflation overshoot, thus giving the Fed every reason to remain hawkish, while the ongoing plunge into protectionism increases the risk of a sharp rise in consumer prices in the next round of 301-related tariffs on Chinese imports. The more hawkish the Fed, the stronger the dollar and the more pressure on emerging markets.

Meanwhile, EM is staring down a potentially disastrous situation in Turkey and the prospect of sanctions on Russian government debt, outcomes that would dent sentiment materially with spillover risks for the entire space.

Additionally, the trade war threatens to undermine global growth, yet another strike against developing economy assets.

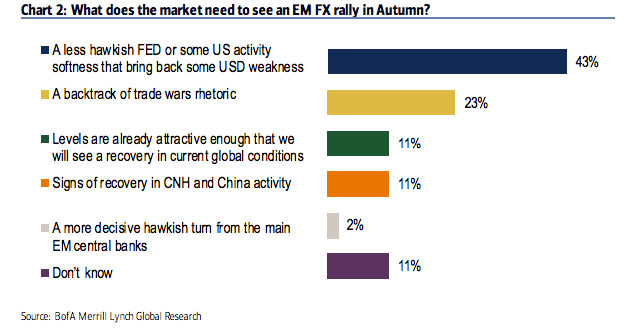

In the latest edition of their FX and rates sentiment survey (conducted from August 3 through August 8), BofAML notes that 43% of respondents (a group that includes 64 fund managers with 335 billion in AUM) believe that dollar weakness, either resulting from a Fed pause or a deceleration in U.S. growth, is the key to reinvigorating the carry trade.

(BofAML)

You’ll note that outcome is seen as potentially more important for EM FX than a deescalation in the trade war. It’s also consistent with the following assessment from the latest note penned by JPMorgan’s Marko Kolanovic:

Regardless of whether this materializes, our view is that a slower pace of hiking is the right thing to do given the divergence of US and international rates, as well as the enormous left tail risk of a potential late-cycle policy error. Should the Fed skip one hike, it would be a risk-on catalyst, lifting EM assets in particular.

As far as the trade war itself goes, 67% of respondents to BofAML’s survey expect things to get modestly worse. Somewhat surprisingly, the percentage of those who think things will get “materially worse” is down sharply from July, even as things have gotten, well, “materially worse” since then.

Leave A Comment