As of June 2008 no Wall Street banking house was predicting a recession, yet by then the Great Recession—–the worst economic downturn since the 1930s—– was already six months old, as per the NBER’s subsequent official reckoning.

Actually, it was already several years old if you concede that the phony housing boom of 2005-2007 was generating merely transient “statistical” GDP, not permanent gains in main street wealth. Even the movie houses showing “The Big Short” have some pretty palpable reminders on that point——not the least being the strip club dancer who owned 5 residential properties, with two adjustable rate mortgages on each.

In fact, by then main street America was crawling with strippers. That is, equity strippers who were repeatedly doing “cash out” refinancings in order to generate between $20,000 and $100,000 or more of mortgage proceeds to spend on vacations, cars, man caves, aspirational leather goods, shoes and apparel, among much else.

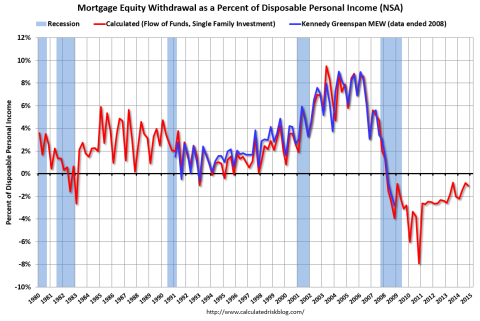

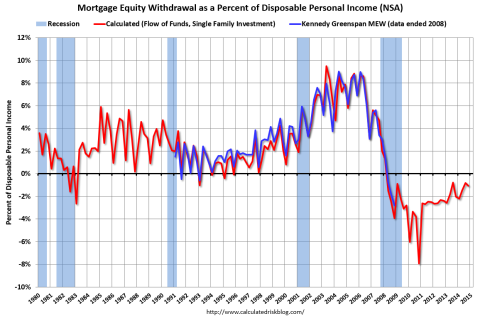

At the peak in 2006-2007, upwards of 10% of personal consumption expenditures were accounted for by MEW (mortgage equity withdrawal). The utter unsustainability of that kind of Potemkin prosperity goes without saying, but the point here is that it was no deep dark secret buried in the economic entrails.

In fact, Chairman Greenspan went to great lengths to publicize the facts of MEW on an up-to-date basis. But he wasn’t trying to warn that the end was near. Unaccountably, he and his Wall Street acolytes concluded that the US economy had become virtually recession proof because of the extra firepower being accorded to household consumption by MEW!

In short, the economic booby trap of MEW was hiding in plain sight and so was the Great Recession. Yet there was nothing at all unusual about the 2008 recession call miss.

Leave A Comment