In February, import prices rose 0.2% in line with the Econoday consensus. Export prices rose 0.3%, slightly more than the consensus estimate of 0.2%.

Revisions took upped January import prices from 0.4% to 0.6% and export prices from 0.1% to 0.2%.

Year-over-year import prices jumped from 3.7% to 4.6% and export prices from 2.3% to 3.1%.

Econoday cites price pressures: “An important sign of pressure comes from the overall year-on-year rate which is at 4.6 percent, its highest level in 5 years, since February 2012.”

That’s a bunch of speculative oil-related nonsense.

As discussed previously, if energy prices continue to rise, there will be price pressures. And if not, there likely won’t.

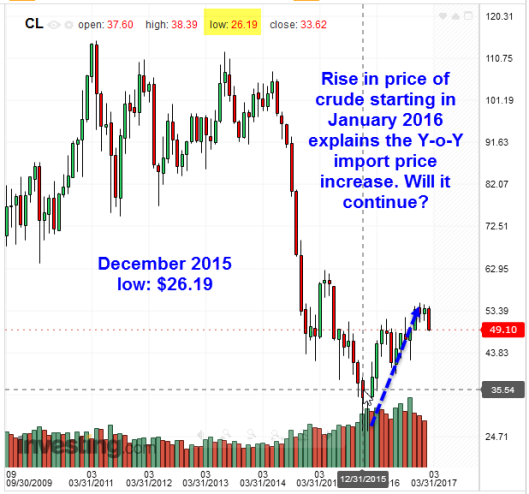

Monthly Crude Chart

Crude Weekly Chart

Those two charts explain year-over-year price pressures and upcoming month-over-month price changes.

Year-over-year inflation will look reasonably strong for some time unless there is a price collapse. The same cannot be said for month-over-month prices.

Inflation Scare or the Real Deal?

I don’t know precisely what crude will do, nor does anyone else. But with rate hikes coming, and GDP estimates diving, I highly doubt oil is about to skyrocket.

Until proven otherwise, I believe, and the charts suggest, that we are in the midst of a price inflation scare.

Leave A Comment