On the day Mario Draghi announced that the ECB would launch a historic corporate bond monetization program, the first of its kind, we said that we expect bond yields to tumble imminently as the market frontruns the ECB’s open-market purchases of corporate bonds and soaks up all available supply in the market. Not even we expected what would happen next though.

As the WSJ writes, four years after ECB President Mario Draghi‘s famous “whatever it takes” speech sparked a decline in the cost of servicing sovereign debt in the Eurozone’s shattered periphery, the same is now seems to be happening for corporate bond issuers in those countries.

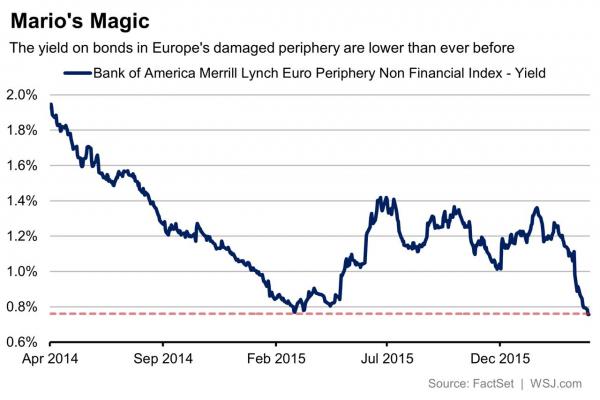

It WSJ writesfor the Eurozone periphery which includes countries like Italy, Spain, Portugal and Ireland (which earlier today issued a 100 Year bond courtesy of the very same ECB), and which touched its lowest yield to maturity ever on Tuesday, at 0.76%.

Once again, Draghi has worked his verbal magic unleashing a buying spree before the ECB has bought even one single bond, all because other buyers are now completely price indiscriminate and fully aware they have the ECB’s backstop.

Perhaps the recent record low yields are a warning: the previous record low yield for the index was 0.78%, which was reached just before the so called bund tantrum of Spring 2015, when credit across Europe sold off, and yields jumped.

However, back then, the buying impetus was driven by the ECB’s sovereign QE program when, unlike now, there was no explicit backstop to corporate bond risk. There is now.

The WSJ also points out that yields on other classes of debt have also declined, but not to the levels recorded in the early months of last year.

Financial companies, whose bonds the ECB will not buy, are still a little way from their lows. In March last year, the yield to maturity of the Bank of America Merrill Lynch index for financial companies in the periphery fell to 1.12%, and it’s now at 1.35%.

The index for non-financial companies in the eurozone but outside the periphery also has a higher average yield than it did in April 2015.

Leave A Comment