The long-awaited recession and resulting resumption of the 2022 bear market that many have been expecting has failed to materialize so far in 2023. In fact, most assets have caught a bid, with the NASDAQ hitting a 52-week high on July 12.

How can this be, and will the rally continue?

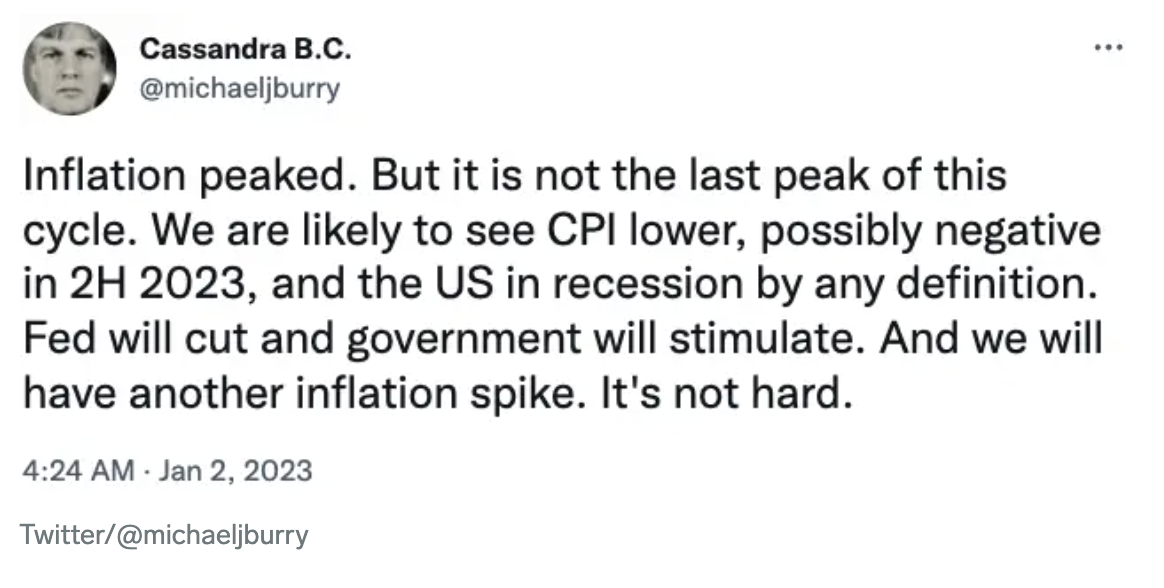

Michael Burry of Big Short fame declared in January that the US could be in recession by late 2023, with CPI lower and the Fed cutting rates (note that today’s CPI print came in much lower than expected, further fueling the recent rally). This would lead to another inflation spike in his view.

Recently independent macro and crypto analyst Lyn Alden explored the topic in a newsletter published this month.

Recently independent macro and crypto analyst Lyn Alden explored the topic in a newsletter published this month.

In the report, Alden examines today’s inflationary environment by contrasting it to two similar but different periods: the 1940s and the 1970s. From this, she concludes that the US economy will likely enter stall speed or experience a mild recession while experiencing some level of persistent inflation. This could mean that markets continue trending upward until an official recession hits.

My July 2023 newsletter is out:https://t.co/gTH0nUyrU8

The topic focus on fiscal dominance, and how large debts and deficits can mute the impact of higher interest rates as a policy tool. pic.twitter.com/qmuzInyYjK

— Lyn Alden (@LynAldenContact) July 2, 2023

The Fed’s inflation fight continues

The important difference between the two periods involves rapid bank lending and large monetized fiscal deficits, which Alden suggests are the underlying factors driving inflation. The former occurred in the 1970s as baby boomers began buying houses, while the latter occurred during World War II as a result of funding the war effort.

The 2020s are more like the 1940s than the 1970s, yet the Fed is running the 1970s monetary policy playbook. This could turn out to be quite counterproductive. As Alden explains:

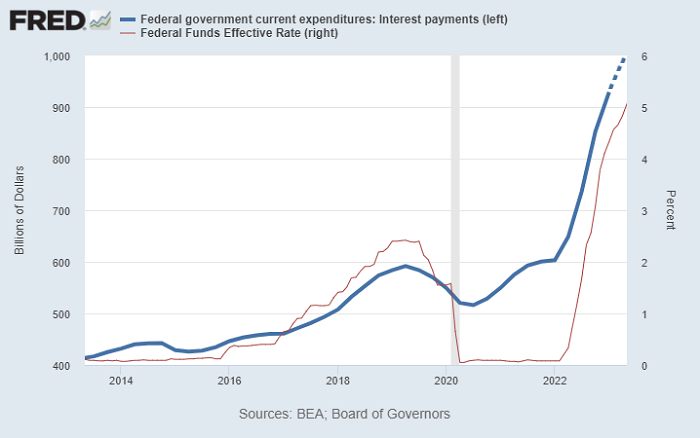

“So as the Federal Reserve raises rates, federal interest expense increases, and the federal deficit widens ironically at a time when deficits were the primary cause of inflation in the first place. It risks being akin to trying to put out a kitchen grease fire with water, which makes intuitive sense but doesn’t work as expected.”

In other words, today’s inflation has been primarily driven by the creation of new federal debt, or what some may call government money printing.

Raising interest rates to calm inflation can work, but it’s meant for inflation that has its roots in an expansion of credit tied to banking loans. While higher rates tame such inflation by making borrowing more expensive and thus reducing loan creation in the private sector, they make fiscal deficits worse by increasing the amount of interest owed on those debts. The federal debt today is over 100% of GDP, compared to just 30% in the 1970s.

In this way, the Fed may be using a tool unfit for the situation, but this hasn’t stopped markets, at least for now.

Big Tech defies recession estimates and propels equities

Despite the Fed’s battle with inflation and market participants’ expectation of an unavoidable recession, the first half of 2023 has been quite bullish for equities, with the rally extending into July. While bonds have sold off again, raising yields to near-2022 highs, risk assets like tech stocks have been soaring.

It’s important to note that this rally has primarily been led by just 7 stocks, including names like Nvidia, Apple, Amazon, and Google. These equities make up a disproportionate weight of the NASDAQ:

Just seven stocks make up 55% of the NASDAQ 100 and 27% of the S&P 500

The distribution has become so lopsided that the NASDAQ will be rebalancing to give these megacaps less weight.

Source: @GoldmanSachs pic.twitter.com/k1xM1wmL2S

— Markets & Mayhem (@Mayhem4Markets) July 13, 2023

Related: Bitcoin mining stocks outperform BTC in 2023, but on-chain data points to a potential stall

Bonds down, crypto and tech up

The rally in tech due in large part to AI-driven hype and a handful of mega cap stocks has also caught a tailwind from an easing in bond market liquidity.

Alden notes how this began late last year:

“But then some things began to change at the start of Q4 2022. The U.S. Treasury began dumping liquidity back into the market and offsetting the Fed’s quantitative tightening, and the dollar index declined. The S&P 500 found a bottom and began stabilizing. The liquidity in sovereign bond markets began easing. Various liquidity-driven assets like bitcoin turned back up.”

A July 11 report from Pantera Capital makes similar observations, noting that real interest rates also have a very different story to tell when compared to the 1970s.

“The traditional markets may struggle – and blockchain might be a safe haven,” in part because “The Fed needs to continue to raise rates,” given that real rates remain at -0.35%, according to the report. They also conclude from this that “There’s still tons of risk in bonds.”

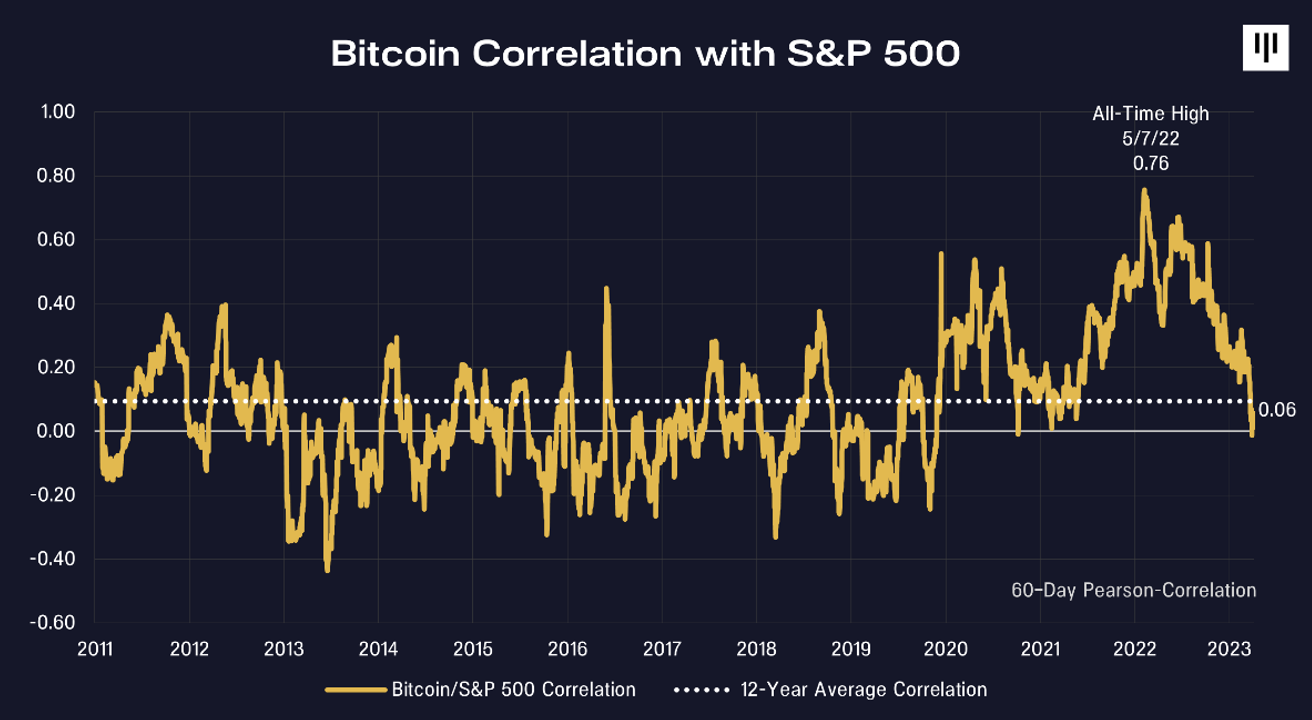

They go on to note that while most other asset classes are sensitive to interest rates, crypto is not. Bitcoin’s correlation to equities during 2022 was driven by the collapse of “over-leveraged centralized entities.” Today, that correlation has reached near-zero levels:

Dan Morehead of Pantera Capital said it well when stating that:

“Having traded 35 years of market cycles, I’ve learned there’s just so long markets can be down. Only so much pain investors can take…It’s been a full year since TerraLUNA/SBF/etc. It’s been enough time. We can rally now.”

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision.

Leave A Comment