Most global equity markets traded lower on the morning after a huge week of rallies that had begun around Ms. Yellen’s Congressional testimony last week. In that testimony, she helped to allay concerns of a completely disconnected Central Bank, as she mentioned data dependency and a non-committal stance towards future rate hikes. This, at the very least, helped to stem the declines that have become commonplace in 2016.

This led to a near 7% incline over the course of four trading days on the SPX500, creating an extremely aggressive trend-channel after a large move lower. As we discussed yesterday, this is on the back of virtually no other positive news outside of that dose of confidence that Chair Yellen delivered last week. Just yesterday we heard the Central Bank of Norway warn that ‘winter is coming,’ alluding to fears of a prolonged global slowdown on the back of lower Oil prices, and the Central Bank of Hungary began to stockpile ammunition. These reports began circulating yesterday, just as we began to break the under-side of the bear-flag formations that have shown up in many global equity markets.

The break of a bear-flag could be significant as it signals a slowdown of the previous retracement, and the potential for a return of the predominant trend, which for global equities right now is lower. Watch the confluent resistance area at 1,950. Should price action continue lower, testing through support at ~1,915 and then ~1,905, short-side positions could become attractive again.

Created with Marketscope/Trading Station II; prepared by James Stanley

The Transmission of Contagion

One of the growing themes this year has been the widely followed correlation between oil prices and stocks. This is somewhat of an abnormality because traditionally, lower oil prices have been a positive for American consumers. So, lower oil prices were thought, for a very long time, to be a bullish thing for stocks. And this made sense to a degree, if a country is importing all of their oil, well oil prices going down means a few more dollars in those consumer’s pockets; just like a tax refund. And if those consumers have a few extra dollars, they’ll likely spend it, and this means better performance for corporates.

Related Posts

Alibaba Smashes All Previous Singles’ Day Sales

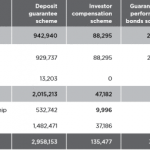

Alibaba Smashes All Previous Singles’ Day Sales French And Italian Bank Deposits Vs. Guarantees: How Safe Is Your Money?

French And Italian Bank Deposits Vs. Guarantees: How Safe Is Your Money? S&P 500 Sell-Off Still In Play But Watch For 2500-2530 Zone

S&P 500 Sell-Off Still In Play But Watch For 2500-2530 Zone SABMiller Accepts ABInBev Offer, Approved Deal Would Create Beer Giant

SABMiller Accepts ABInBev Offer, Approved Deal Would Create Beer Giant- E

Lies, Damned Lies, Corporate “Earnings” And “Volatile Markets

- Taiwan using China trade deal to sell foreign FTAs

Leave A Comment